![Understanding Solo 401(k) Plans [2026]](https://scarletoakfs.com/wp-content/uploads/2025/01/Understanding-Solo-401k-Plans-2025-h.jpg)

As of 2023, 27.1 million US businesses were businesses with no employees.[1] Owners of businesses have options to save for retirement with Traditional and Roth IRAs. But these types of individual accounts have significantly lower contribution limits than employer sponsored retirement plans like 401(k)s, 403(b)s, 457 plans, or even SIMPLE IRAs or Simple 401(k), which may leave many small business owners with a lack of income at retirement. Solo 401(k) plans allow owners who are the only employee to save as much as if they were working for an outside employer rather than themselves. [2],[3]

Key aspects of solo 401(k) plans:

- The employee portion of the contributions is either pre- or post-tax. As a single-person 401(k) plan, the owner can set up the plan with their tax needs in mind. With a Traditional solo 401(k), they could lower their tax burden in the present with pre-tax contributions but pay taxes when they withdraw the money later. And with the Roth version, they would face no taxes at distribution but pay taxes on the income in the present.

- The Solo 401(k) Profit Sharing Contributions or the Employer Contributions can only be made as pre-tax contributions. 2,3,[4]

-

Solo 401(k) plans must be opened under an Employer Identification Number (EIN). You cannot open a Solo 401(k) using your Social Security number.

Employer (Profit-Sharing) Contribution Limits: As the employer, you can contribute up to 25% of your compensation (net self-employment income for sole proprietors), up to the combined limit shown above.

- Contributions can be made until the tax filing deadline for that tax year (April 15th or October 15th if you file for an extension). However, the plan must be established before the end of a calendar year to contribute to that year. 3

- Employer contributions for sole proprietors are based on net self-employment income after deducting one-half of self-employment tax and the employee deferral. [16]

- Part-Time Worker Eligibility: The SECURE 2.0 Act reduces the service requirement for part-time workers to become eligible for 401(k) plans from three consecutive years with at least 500 hours of service to two years, effective in 2025. Although Solo 401(k) plans typically cover self-employed individuals without employees, this change is relevant for those considering hiring part-time staff.

- Beginning in 2023, employers may allow Roth employer contributions (profit sharing) if the plan supports it.[17]

- Automatic Enrollment Requirement: Starting in 2025, the SECURE 2.0 Act mandates that newly established 401(k) and 403(b) plans must automatically enroll eligible employees, with initial contribution rates set between 3% to 10% of compensation. Starting in 2025, small businesses, including self-employed individuals (Solo 401(k) sponsors), may be eligible for a tax credit of up to $500 annually for the first three years when they implement an automatic enrollment feature in a new or existing 401(k) or 403(b) plan. While Solo 401(k) plans with no employees are not mandated to comply with the automatic enrollment rule, adding automatic enrollment could still qualify for the tax credit if employees are hired in the future.

- A Solo 401(k) must file Form 5500-EZ once plan assets exceed $250,000, or if the plan terminates.

- Investment options include individual stocks, mutual funds, ETFs, annuities, UITs, etc. Investment vehicles are prohibited in solo 401(k)s, including antiques/collectibles (artwork, gems, wines, etc.) and most coins. [8]

- With all investment accounts, you expose some or all your invested money to loss for the chance to earn a higher profit. Investment gains hinge on an ongoing and long-term investment strategy that uses your risk tolerance and diversification to mitigate some risks. Even with these in place, you are exposing your money to loss.[9]

- The earliest you can take penalty-free withdrawals is 59 ½; the penalty is an extra 10% on top of the taxes collected. However, there are some exemptions to the early withdrawal penalty- if you are permanently and totally disabled, if you lose your job at 55 or older, if you have medical expenses that exceed 10% of your modified adjusted gross income, with some divorce settlement types and if you die.2

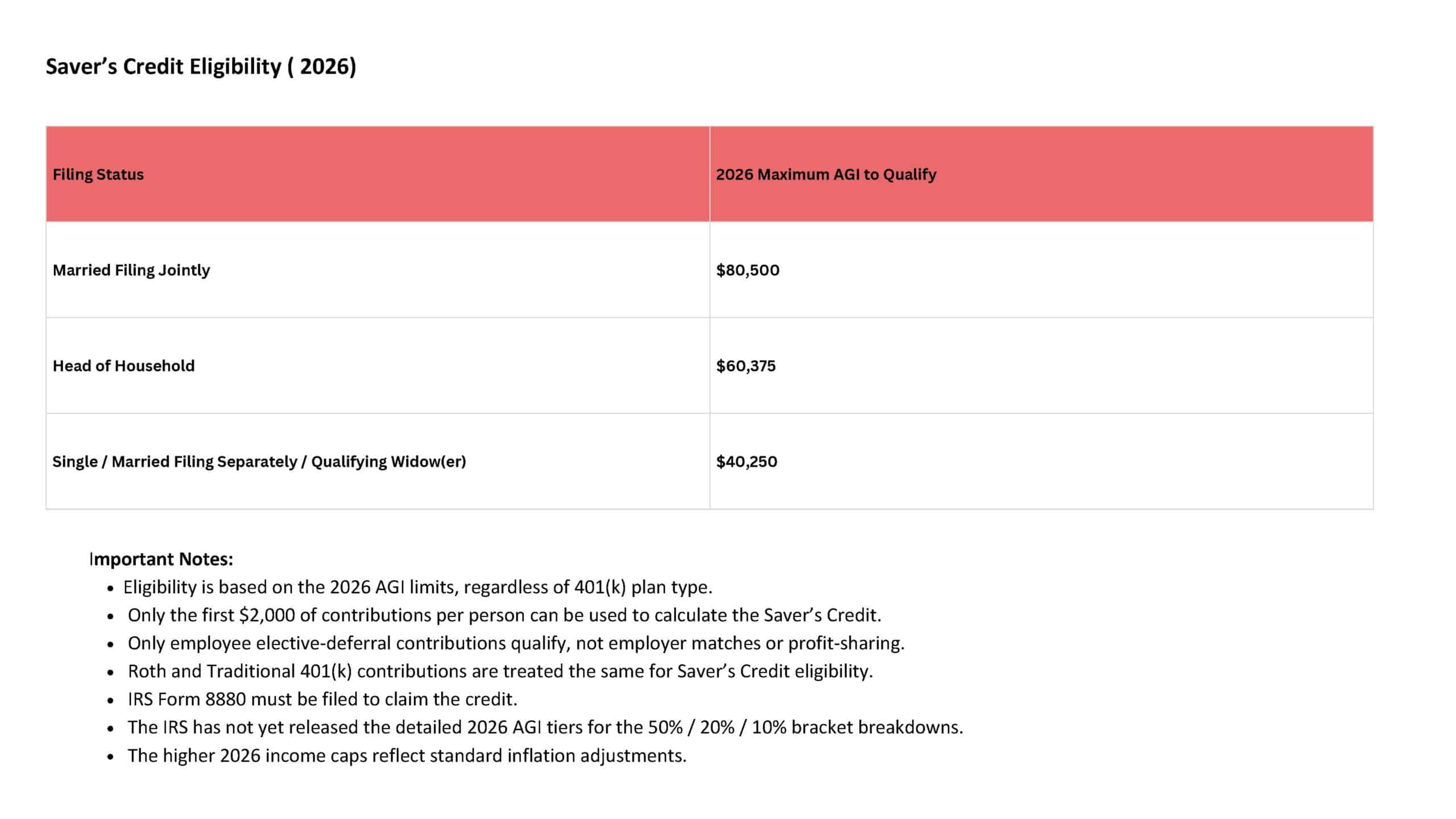

The Saver’s Credit provides a tax benefit for contributing to eligible retirement accounts, helping lower- and moderate-income earners boost their long-term savings.

Eligible Contribution Types

Employee contributions to the following accounts qualify:

• Traditional or Roth IRAs

• 401(k) plans — including Traditional, Roth, Safe Harbor, Solo/Individual, and SIMPLE 401(k)

• 403(b) plans

• 457(b) governmental plans

• SIMPLE IRAs

• SEP IRAs

(Only employee elective-deferral contributions qualify—not employer matches or profit-sharing.)

High Earners (New Roth Catch-Up Requirement for Solo 401(k)s: Beginning January 1, 2026, Solo 401(k) participants with prior-year Social Security (W-2) wages over $145,000 must make all catch-up contributions as Roth, but only if the plan includes a Roth feature.

If the Solo 401(k) plan does not allow Roth contributions, high earners will not be able to make catch-up contributions.

Important for Solo 401(k) Owners:

• This rule only applies if the business owner is paid W-2 wages (S-Corp or C-Corp).

• Sole proprietors and single-member LLCs taxed as sole proprietorships do not have W-2 wages, so the $145,000 threshold does not apply to them. Their catch-up contributions may remain pre-tax as usual.

Born before 7/1/1949 → 70½

Born 7/1/1949–1950 → 72

Born 1951–1958 → 73

Born 1960 or later → 75

Born in 1959 → Federal clarification pending (age 73 or 75)

Roth Solo 401(k) accounts do not require RMDs starting in 2024.[10],[11]

- As the only participant within the fund, you can build a plan that allows both hardship withdrawals and loans.[12]

- Solo 401(k) plans are not required to perform nondiscrimination tests (NDTs) because they are only allowed for a business without employees, and therefore, there is no fairness standard to check. 2

- Fees vary from plan to plan. It is crucial to understand how much you are paying in fees.

- If you structure it into your plan, you can accept rollovers from other retirement accounts, including SEP IRAs and traditional 401(k)s. You can roll over your solo 401(k) assets into another 401(k) or an IRA. Like with all retirement accounts, only if the new accounts match the tax designation of the original account- pre-tax account to pre-tax account and post-tax to post-tax. 2

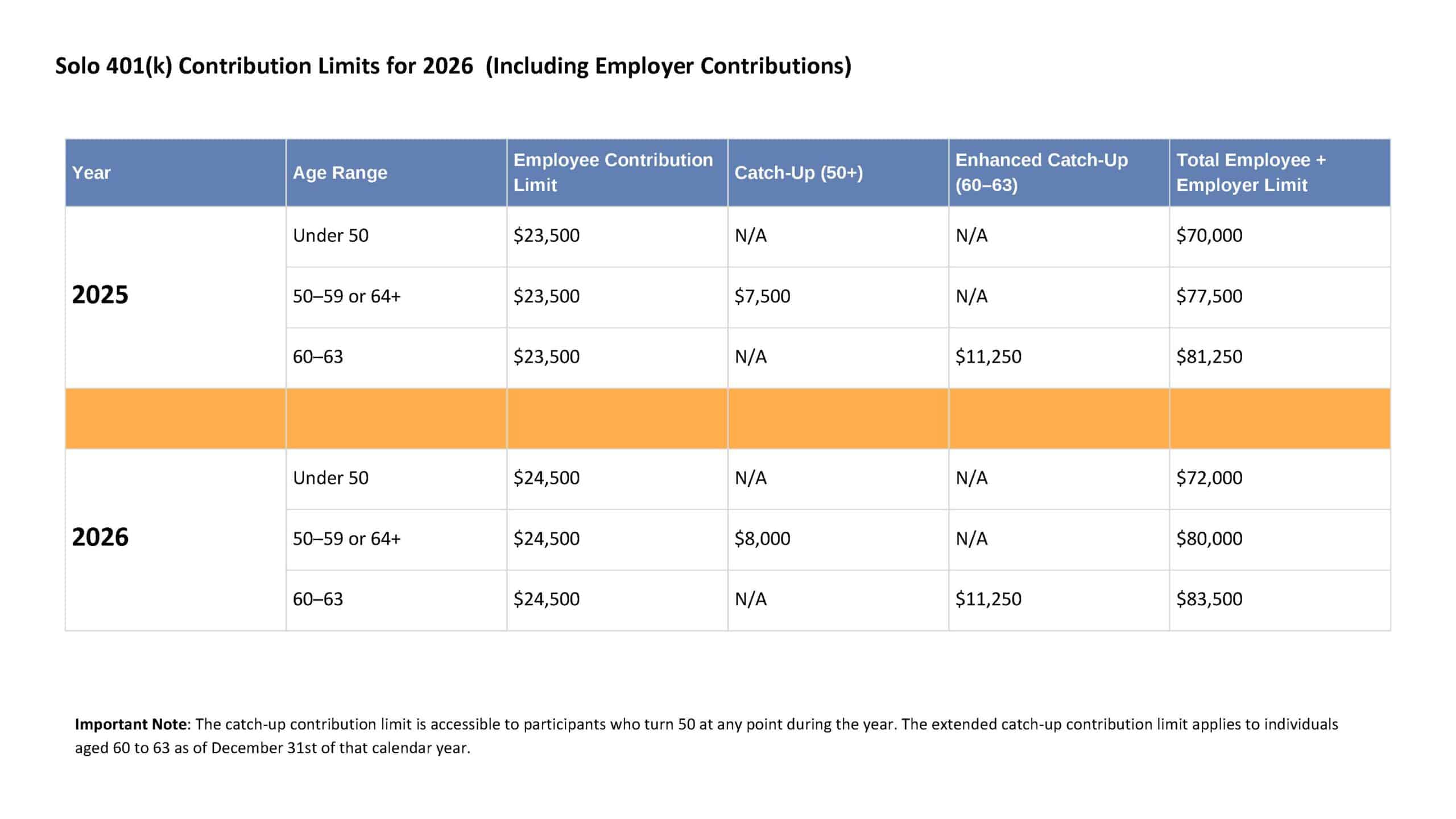

- Suppose the business owner also works at a job that offers an employer sponsored retirement plan (as an example- they sold freelance artwork while maintaining outside employment). If the business owner also contributes to a retirement plan at another job, employee elective-deferral limits apply across all plans combined—$23,500 plus a $7,500 catch-up for those age 50+ in 2025, and $24,500 plus an $8,000 catch-up for those age 50+ in 2026—while employer contributions remain separate. [13],[14],[15]

- You can take a low-interest loan on Solo 401(k) accounts, up to $50,000 or 50% of your account balance. The loan is for a 5-year maximum term. The period can be extended if the loan is used to purchase a primary residence. Some plans don’t let you contribute to your account until the loan is paid back. Interest charges go directly back into your retirement account. If you fail to repay the loan, it is considered a distribution and taxed accordingly, including early distribution penalties if applicable based on your age.6

We want to help you with your retirement planning. Scarlet Oak Financial Services can be reached at 800.871.1219 , or you can contact us here. To sign up for our newsletter with the latest economic news, click here.

Sources:

[1] https://www.forbes.com/advisor/business/small-business-statistics/#:~:text=Yet%2C%20despite%20the%20fact%20that,businesses%20employ%2061.7%20million%20workers.

[2] https://www.fidelity.com/learning-center/personal-finance/retirement/self-employed-401k

[3] https://www.nerdwallet.com/article/investing/what-is-a-solo-401k

[4] https://www.irafinancialgroup.com/learn-more/solo-401k/2022-solo-401k-contribution-limit-changes/

[5] https://www.shrm.org/resourcesandtools/hr-topics/benefits/pages/2023-irs-401k-contribution-limits.aspx

[6] https://www.irs.gov/newsroom/401k-limit-increases-to-23000-for-2024-ira-limit-rises-to-7000

[7] https://fitaxguy.com/2024-solo-401k-update/

[8] https://royallegalsolutions.com/prohibited-solo-401k-investments-what-you-cant-invest-in-with-a-solo-401k

[9] https://www.investor.gov/sites/investorgov/files/2019-02/Saving-and-Investing.pdf

[10] https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-required-minimum-distributions-rmd

[11] https://www.tiaa.org/public/support/faqs/required-minimum-distributions

[12] https://ira123.com/solo-401k-loan/

[13] https://finance.zacks.com/can-contribute-401k-simple-ira-same-year-2907.html

[14] https://www.whitecoatinvestor.com/multiple-401k-rules/

[15] https://www.irs.gov/newsroom/401k-limit-increases-to-22500-for-2023-ira-limit-rises-to-6500#:~:text=Highlights%20of%20changes%20for%202023,to%20%246%2C500%2C%20up%20from%20%246%2C000

[17] https://www.irs.gov/pub/irs-drop/n-24-02.pdf

Congress.gov | Library of Congress

https://www.solo401k.com/

https://www.irs.gov/newsroom/401k-limit-increases-to-24500-for-2026-ira-limit-increases-to-7500https://www.irs.gov/pub/irs-drop/n-25-67.pdf

https://www.irs.gov/pub/irs-drop/n-25-67.pdf

This material has been prepared for informational purposes To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on individual circumstances.