![Understanding 457 Plans [2026]](https://scarletoakfs.com/wp-content/uploads/2023/01/Understanding-403b-Plans-2025.jpg)

457 plans are offered by state and local governments and some non-profits. These are pre-tax accounts; just like 401(k) and 403(b) plans, contributions come from your paycheck before income tax is withheld, but you will pay taxes when you withdraw the money in retirement. But in the meantime, the account is allowed to grow tax-deferred. There are two types of 457 plans- 457(b) offered to state and local government employees, and 457(f) offered to highly compensated government and select non-government employees.[1]

Key aspects of 457(b) plans:

-

Governmental vs. Tax-Exempt 457(b) Plans: It is important to distinguish between governmental and tax-exempt (non-governmental) 457(b) plans because the rules differ significantly. These differences affect rollover options, Roth availability, catch-up eligibility, funding protections, and creditor exposure.

-

Governmental 457(b) Plans: Governmental 457(b) plans have more flexibility and stronger protections for participants. These plans may offer Roth contributions if the employer includes this feature. Governmental 457(b) balances can be rolled over into IRAs, 401(k) plans, 403(b) plans, or another governmental 457(b), giving participants more options when changing employers. These plans may also offer the special “double limit” catch-up provision, allowing eligible participants within three years of normal retirement age to contribute up to twice the annual contribution limit. In addition, governmental 457(b) plans must be funded, and plan assets are held in trust for the employee, meaning they are protected from employer creditors. [21], [22]

- Tax-Exempt 457(b) Plans: Tax-exempt 457(b) plans (offered by private nonprofits) operate under much stricter limits. These plans cannot offer Roth contributions and do not permit rollovers to IRAs, 401(k)s, or 403(b)s. The only eligible rollover destination is another tax-exempt 457(b) plan. Tax-exempt 457(b) plans also do not allow the double limit catch-up, meaning participants are limited to the standard annual contribution and, if eligible, the age 50+ catch-up. These plans must remain unfunded to maintain their ERISA-exempt status, which means the assets remain the property of the employer until paid out. As a result, participant balances are subject to the claims of the employer’s general creditors in the event of lawsuits, bankruptcy, or insolvency. [21], [22]

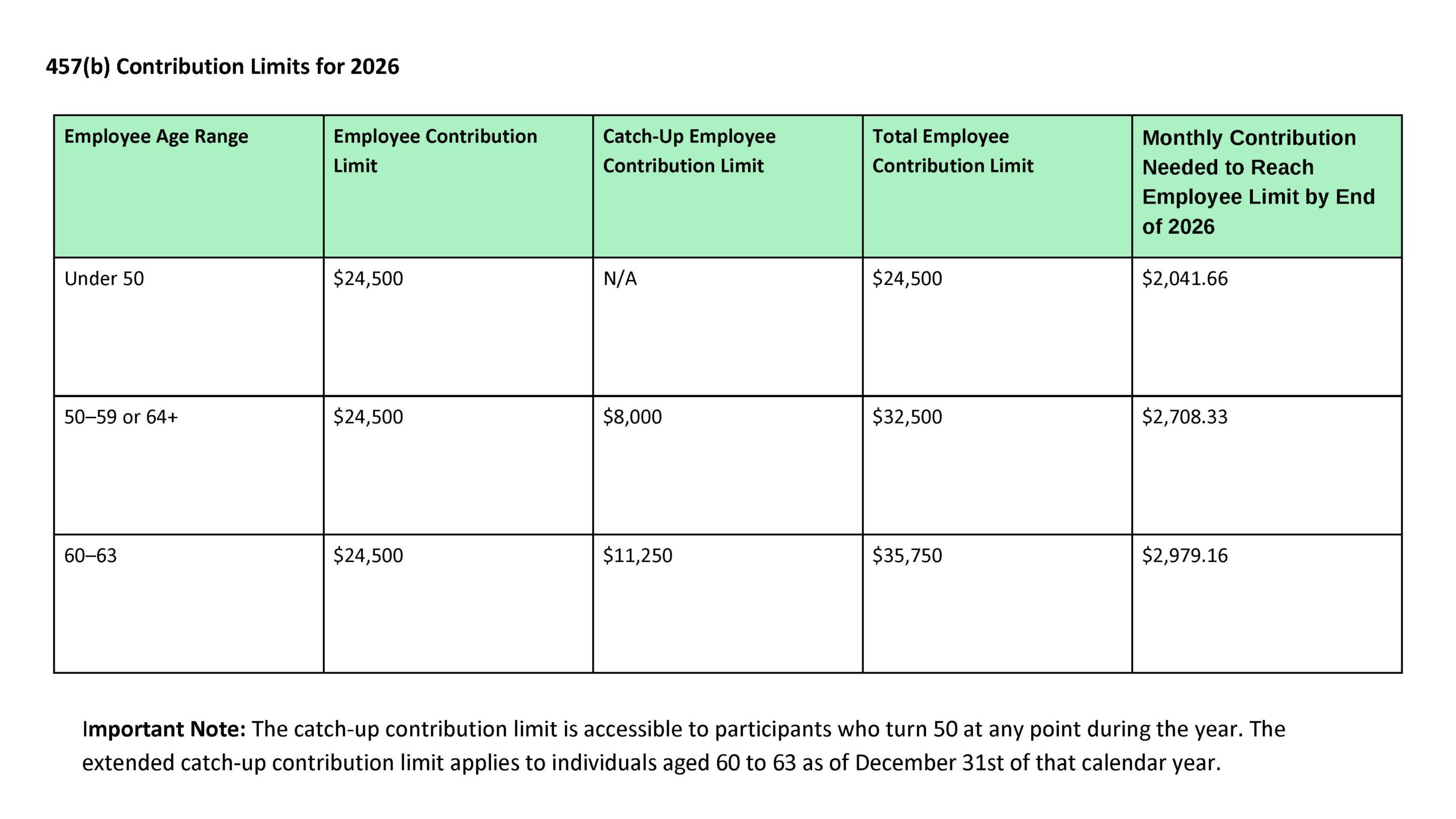

Double Limit Catch-Up (Governmental 457(b) Only): 457(b) governmental plans continue to offer the “double limit catch-up” provision, allowing eligible participants to significantly increase retirement contributions.

Eligibility:

Participants within three years of the plan’s defined “normal retirement age” may use this catch-up rule. The normal retirement age cannot exceed 70½ and must align with the employer’s pension/benefits structure.

Contribution Limit (2026):

Up to twice the annual deferral limit.

Annual limit = $24,500 → Double limit = $49,000

Calculation Basis:

The increased limit is the lesser of:

-

Twice the deferral limit (e.g., $47,000 in 2025, $49,000 in 2026), or

-

The limit plus unused elective deferrals from prior eligible years.

Important:

You cannot use both the age 50+ catch-up and the double limit catch-up in the same year. Not all plans allow this—participants must confirm availability with their plan administrator.

For 2026, this allows eligible employees to contribute:

-

$24,500 to a 457(b) plan, and

-

$24,500 to a 401(k) or 403(b) plan

Total potential employee deferrals in 2026: $49,000, before any catch-up contributions.

This separation of limits is unique to 457(b) plans. Unlike 401(k) and 403(b) plans, which share a combined elective deferral limit when offered by the same employer, governmental 457(b) plans maintain their own independent limit and do not reduce contribution room in a 401(k) or 403(b).

This feature is especially valuable for employees who work for two employers concurrently (for example, a public-sector job plus private employment) or employees whose public-sector employer offers both plan types. [6], [23]

Important Considerations:

- Mutual Exclusivity with Age 50+ Catch-Up: Participants cannot use both the age 50+ catch-up provision and the double limit catch-up in the same year. They must choose the option that provides the higher contribution limit.

- Plan Specifications: Not all 457(b) plans offer the double limit catch-up provision. Participants should consult their plan documents or speak with their plan administrator to confirm availability and specific eligibility criteria.

This provision is designed to help employees nearing retirement age accelerate their savings, especially if they had not maximized contributions in earlier years. By understanding and utilizing the double limit catch-up, eligible participants can enhance their retirement readiness.

Secure Act 2.0: Required Minimum Distribution (RMD) Age for 457(b) Plans: Governmental 457(b) plans must follow the federal RMD schedule established under the SECURE Act and SECURE 2.0. The age at which RMDs begin depends on your birth year:

Born before 7/1/1949 → RMD age 70½

Born 7/1/1949–1950 → RMD age 72

Born 1951–1958 → RMD age 73

Born 1960 or later → RMD age 75

Born in 1959 → Federal clarification pending (age 73 or 75)

Important Notes for 457(b) Plans

-

RMDs apply to governmental 457(b) accounts, even if you continue working for the employer after reaching RMD age—unless the employer allows the “still-working exception.”

-

Roth 457(b) accounts (starting in 2024) are exempt from RMDs, aligning with Roth IRAs.

-

If you roll a pre-2024 Roth 457(b) balance into a Traditional IRA, that portion becomes subject to RMDs.

-

Rolling a Roth 457(b) into a Roth IRA preserves RMD-free treatment.[11],[12]

- If you leave an employer, you can take your money with you.[7]

- 457(b) plans investment options are generally limited to annuities and mutual funds.

- Governmental 457(b) plans may also offer Roth contribution options, depending on the plan. Tax-exempt 457(b) plans cannot offer Roth contributions, as they are restricted to pre-tax deferrals only.[8],[9]

- Penalty-Free Withdrawals at Any Age: One of the most distinctive advantages of 457(b) plans is that they do not impose the 10% early withdrawal penalty—at any age. This makes 457(b)s especially valuable for workers who often retire earlier than traditional retirement timelines, including:

-

Police

-

Firefighters

-

EMTs

-

Other municipal and public safety workers

-

Employees in high-risk or shift-based roles who typically retire in their 40s or 50s

-

- Withdrawals from a 457(b) are still subject to regular income tax, but they are never penalized, unlike 401(k) and 403(b) plans. This feature allows early retirees—such as firefighters who may work from age 21 to 46—to access their retirement funds well before age 59½ without added tax costs.[10]

- You can take a low-interest loan on 457(b) accounts, up to $50,000 or 50% of your account balance. You can take out the total amount if your balance is $10,000 or less. You will have to pay back the loan within five years (this period may be extended if the money is used to buy a primary home) or leave that job, or it becomes taxable income. The payments will most likely be held back from your paycheck.[13]

Key aspects of 457(f) plans:

- A critical tax detail for 457(f) plans is how and when taxes apply. FICA taxes (Social Security and Medicare) are due at vesting, when the risk of forfeiture lapses, even though the money may not be distributed yet. Income taxes are due at the time of distribution, which may occur months or years after vesting. This distinction is especially important for highly compensated employees, as it can create tax timing issues that must be planned for carefully. [24]

- Whether or not you move on to a new employer, your money will stay with this plan. And if you don’t meet the terms of your employment contract, you can forfeit the entire account.9

- 457(f) plan investment options are broader than 457(b) and range from fixed or variable annuities, mutual funds, and even life insurance.9

- With the 457(f) plans, you can also fund a 401(k) or IRA. 9,[16]

- The employer owns the 457(f)-account money until it is distributed, and often you, as the employee, are 0% vested until their distribution. However, some plans offer an incremental vesting schedule. In addition, because your employer owns it, these funds are available to the company’s general creditors in the event of litigation or bankruptcy.[17]

- You can make penalty-free withdrawals at any age if your employment contract is met. 11

- Loans are not available. 11

- Required Minimum Distributions (RMDs) rules do not apply to 457(f) plans. 11

- It is vital to understand the details of your specific plan so as not to risk forfeiture. 11

Both

- With all investment accounts, you expose some or all your invested money to loss for the chance to earn a higher profit. Investment gains hinge on an ongoing and long-term investment strategy that uses your risk tolerance and diversification to mitigate some risks. Even with these in place, you are exposing your money to loss.[18]

- Matching is not standard for these types of plans. Employers often limit their role and do not provide employer contributions to the plan to remain exempt from ERISA rules. Employee Retirement Income Security Act (ERISA) of 1974 rules were implemented to safeguard employees who participate in employer-run retirement plans.[19]

- Profit-sharing, where a company offers stock options to its employees, is not available with these types of plans since these organizations are non-profit or governmental.[20]

- The distributions are reported on a W-2, not a 1099, unless a beneficiary requests the distribution; because of the distribution method, you will pay Social Security tax on all distributions. 11

If you would like to explore additional retirement investment accounts that could work for your personal goals, Scarlet Oak Financial Services can be reached at 800.871.1219, or you can contact us here. To sign up for our newsletter with the latest economic news, click here.

Sources:

[1] https://www.investopedia.com/terms/1/457plan.asp

[2] https://www.irs.gov/newsroom/401k-limit-increases-to-23000-for-2024-ira-limit-rises-to-7000

[3] https://www.investopedia.com/terms/1/457plan.asp

[4] https://www.irs.gov/newsroom/401k-limit-increases-to-22500-for-2023-ira-limit-rises-to-6500#:~:text=Highlights%20of%20changes%20for%202023,to%20%246%2C500%2C%20up%20from%20%246%2C000.

[5] https://www.irs.gov/retirement-plans/comparison-of-tax-exempt-457b-plans-and-governmental-457b-plans

[6] https://www.forbes.com/advisor/retirement/457b-plan/

[7] https://www.edwardjones.com/us-en/investment-services/account-options/retirement/457-plans

[8] https://www.forbes.com/advisor/retirement/457b-plan/

[9] https://www.irs.gov/retirement-plans/irc-457b-deferred-compensation-plans

[10] https://www.investopedia.com/ask/answers/021616/are-457-plan-withdrawals-taxable.asp

[11] https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-required-minimum-distributions-rmd

[12] https://www.tiaa.org/public/support/faqs/required-minimum-distributions

[13] https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-loans

[14] https://money-zine.com/financial-planning/retirement/457f-plans/

[15] https://www.irs.gov/pub/irs-tege/chap601.pdf (36 page)

[16] https://www.investopedia.com/ask/answers/100314/what-difference-between-401k-plan-and-457-plan.asp

[17] https://hanysbenefits.com/resources/docs/faqs/hbs_faqs_457f_457b.pdf

[18] https://www.investor.gov/sites/investorgov/files/2019-02/Saving-and-Investing.pdf

[19] https://www.investopedia.com/terms/1/457plan.asp

[20] https://www.investopedia.com/articles/personal-finance/111615/457-plans-and-403b-plans-comparison.asp

[21] https://www.irs.gov/retirement-plans/comparison-of-tax-exempt-457b-plans-and-governmental-457b-plans

[22] https://www.irs.gov/retirement-plans/issue-snapshot-section-457b-plan-of-governmental-and-tax-exempt-employers-catch-up-contributions

[23] https://www.irs.gov/retirement-plans/how-much-salary-can-you-defer-if-youre-eligible-for-more-than-one-retirement-plan

[24] https://www.truckerhuss.com/2022/07/fica-tax-withholding-and-reporting-for-section-457b-and-457f-nonqualified-deferred-compensation-plans/?utm_source=chatgpt.com

https://tickertape.tdameritrade.com/retirement/457b-vs-403b-retirement-plans-17857

https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-loans

https://www.edwardjones.com/us-en/investment-services/account-options/retirement/457-plans

https://www.irs.gov/newsroom/401k-limit-increases-to-24500-for-2026-ira-limit-increases-to-7500

https://www.irs.gov/pub/irs-drop/n-25-67.pdf

This material has been prepared for informational purposes. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on individual circumstances.