![Understanding Roth IRAs [2026]](https://scarletoakfs.com/wp-content/uploads/2025/01/Understanding-Roth-IRAs-2025.jpg)

A Roth Individual Retirement Account (Roth IRA) is a personal account that allows you to save for your retirement on top of employer sponsored plans like 401(k), 403(b), and 457 plans and then make tax-free withdrawals.

Key aspects of Roth IRAs:

- Roth contributions are post-tax contributions taxed when you earn the income, not when the retirement distribution is made. So, say you earn $2000 per paycheck and contribute $200 as a Roth contribution. You will still pay taxes on the $2000. Whereas if you had made a traditional IRA contribution of $200, you’d pay taxes on an adjusted paycheck of $1800.[1]

- Once you contribute money to a Roth IRA, your investments can grow tax-free within the account. This means you won’t owe taxes on the capital gains, dividends, or interest earned as long as the funds remain in the Roth IRA. You were taxed before the funds entered the account. 1

- With all investment accounts, you expose some or all your invested money to loss for the chance to earn a higher profit. Investment gains hinge on an ongoing and long-term investment strategy that uses your risk tolerance and diversification to mitigate some risks. Even with these in place, you are exposing your money to loss.[2]

- Roth IRAs follow two separate five-year rules that determine whether earnings and converted funds can be withdrawn without taxes or penalties. For earnings to be tax-free, the account must have been open for at least five tax years and the withdrawal must meet a qualifying event such as turning age 59½, disability, death, or the first-time homebuyer exception. Roth conversions also have their own five-year clock, and withdrawing converted funds before age 59½—or before that conversion’s five-year period has passed—may trigger the 10% penalty. These rules make understanding timing essential before taking Roth IRA distributions. [10]

- Investment options include individual stocks, mutual funds, ETFs, annuities, UITs, etc. Investment vehicles not allowed in IRAs are Life Insurance, types of Derivatives Positions, antiques/collectibles, personal real estate, and most coins.[4]

- Only earned income can be contributed to a Roth IRA. You cannot contribute from alimony (nontaxable), child support, Social Security retirement benefits, or unemployment benefits.[5]

- Investment control is either by your chosen institution or advisor or can be self-directed. With this account, you must know your risk tolerance and diversification strategy. These are especially important if you are self-directed and need to make changes to your investments as you make changes to your life and risk tolerance.

- Roth IRAs can accept rollovers from other Roth-designated retirement accounts—including Roth 401(k), Roth 403(b), and Roth 457(b) plans. These rollovers retain their tax-free withdrawal potential as long as the Roth IRA’s five-year rule is satisfied. Roth IRAs cannot be rolled back into employer retirement plans. [8], [12]

- A Backdoor Roth IRA is an IRS-approved strategy that allows high-income earners to fund a Roth IRA even when their income exceeds the Roth contribution limits. This method works by contributing to a Traditional IRA—often a non-deductible contribution—and then converting those funds to a Roth IRA. Because Traditional IRAs and Roth IRAs are aggregated for the IRS pro-rata rule, taxes may apply on the conversion if any pre-tax IRA money exists. Individuals who use this strategy must file IRS Form 8606 to document their after-tax basis and track the taxation of converted funds. [13]

- Fees vary from institution to institution. It is important to understand how much you are paying in fees.

- Roth IRA withdrawals follow a unique ordering rule that affects how taxes and penalties apply. Contributions can be withdrawn at any time, at any age, without taxes or penalties because they were made with after-tax dollars. Earnings, however, may be subject to taxes and the 10% early withdrawal penalty if the withdrawal is not considered a qualified distribution. Earnings become tax- and penalty-free only when the account has been open for at least five tax years and the withdrawal occurs after age 59½, disability, death, or for a first-time home purchase (up to $10,000). If a withdrawal does not meet these conditions, certain IRS exceptions—such as disability, qualified education expenses, medical costs above 10% of AGI, health insurance while unemployed, IRS levy, qualified reservist distributions, and the domestic abuse exception beginning in 2024—can eliminate the penalty but may not eliminate applicable taxes on earnings.[7], [10]

- Starting in 2024, individuals may withdraw up to $10,000 from a Roth or Traditional IRA without the 10% early withdrawal penalty if the distribution is taken due to domestic abuse. The withdrawn amount may be repaid to the IRA within three years to restore its tax-advantaged treatment. This provision adds a new category of penalty-free withdrawals under the SECURE 2.0 Act. [11]

- Roth IRAs are the only retirement account that does not require minimum distributions during the account owner’s lifetime. This allows funds to remain invested and continue growing tax-free indefinitely. Beneficiaries, however, may still be subject to distribution rules under the SECURE Act.

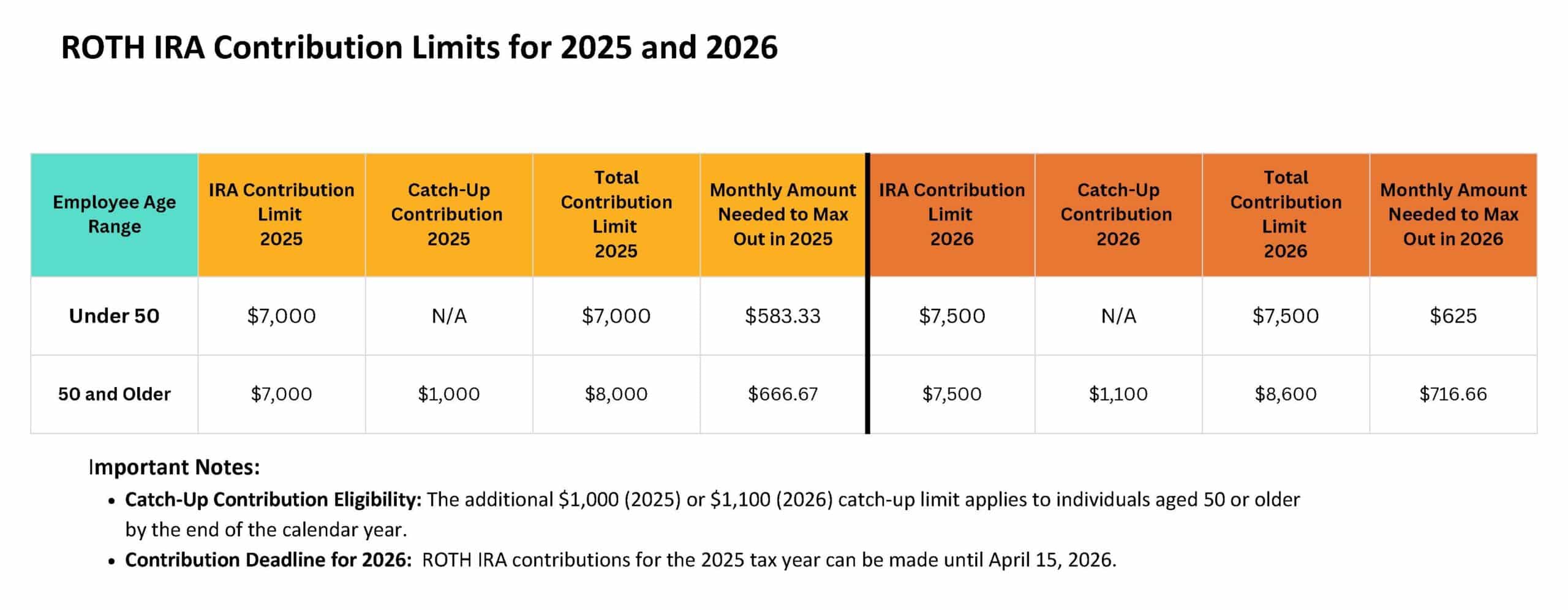

- If you have both a Traditional IRA and a Roth IRA, the total amount you can contribute across all your IRA accounts is capped at the annual IRS limit—up to the standard contribution amount, with a higher limit available once you reach age 50.[9]

- If you contribute more than the annual limit or your income exceeds the Roth IRA eligibility limits, the IRS assesses a 6% penalty each year on the excess amount. The excess can be corrected by withdrawing it (and related earnings) before the tax filing deadline or by recharacterizing it to a Traditional IRA if eligible. If you make a Roth IRA contribution but later discover your income is too high, the IRS still allows you to “recharacterize” the contribution to a Traditional IRA. [14]

If you would like to explore additional retirement investment accounts that could work for your goals, Scarlet Oak Financial Services can be reached at 800.871.1219, or you can contact us here. To sign up for our newsletter with the latest economic news, click here.

Sources:

[1] https://www.investopedia.com/terms/r/rothira.asp

[2] https://www.investor.gov/sites/investorgov/files/2019-02/Saving-and-Investing.pdf

[3] https://www.irs.gov/newsroom/401k-limit-increases-to-23000-for-2024-ira-limit-rises-to-7000

[4] https://www.investopedia.com/articles/personal-finance/103114/roth-iras-investing-and-trading-dos-and-donts.asp

[5] https://www.investopedia.com/articles/personal-finance/081615/basics-roth-ira-contribution-rules.asp

[6] https://www.irs.gov/newsroom/401k-limit-increases-to-23000-for-2024-ira-limit-rises-to-7000

[7] https://www.schwab.com/ira/roth-ira/withdrawal-rules

[8] https://www.irs.gov/pub/irs-tege/rollover_chart.pdf

[9] https://www.investopedia.com/ask/answers/03/081503.asp

[10] https://www.irs.gov/publications/p590b

[11] https://www.irs.gov/pub/irs-drop/n-24-55.pdf

[12] https://www.irs.gov/pub/irs-tege/rollover_chart.pdf

[13] https://www.irs.gov/forms-pubs/about-form-8606

[14] https://www.irs.gov/publications/p590a

https://www.irs.gov/newsroom/401k-limit-increases-to-23500-for-2025-ira-limit-remains-7000

https://www.irs.gov/pub/irs-drop/n-25-67.pdf

https://www.irs.gov/newsroom/401k-limit-increases-to-24500-for-2026-ira-limit-increases-to-7500

This material has been prepared for informational purposes. *To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on individual circumstances.