![Understanding Rollover IRAs [2026]](https://scarletoakfs.com/wp-content/uploads/2025/01/Understanding-Rollover-IRAs-2025-h.jpg)

A Rollover Individual Retirement Account (IRA) is a personal account that allows you to move employer sponsored plans like 401(k), 403(b), and 457 plan monies into it.[1] Though it has many of the same features that a Traditional IRA has, there are a couple of key differences:

-

-

- Some employer sponsored plans only accept money from another employer sponsored plan. A Rollover IRA would be the way to go if you wanted a personal account that could always be converted into an employer plan. A Rollover IRA can be a holding account for these assets. You might not immediately work for an employer who has an employer sponsored plan after you have left a job, but you could still want control of your retirement account, pay fewer fees, which IRAs tend to have, and have more investment choices.[2]

- Creditors cannot touch employer sponsored accounts. Accounts like 401(k), 403(b), and 457 have unlimited creditor protection, while Traditional IRAs only have protection up to $1,512,350 between April 1, 2022, and March 31, 2025. Rollover IRAs also have unlimited protection. But if you contribute personal (non-rollover) money to a Rollover IRA, it may lose its ERISA-level unlimited creditor protection, because the account is no longer purely rollover funds. 2,[3]

-

Key aspects of Rollover IRAs:

- They are a pre-tax investment account.[4]

- With all investment accounts, you expose some or all your invested money to loss for the chance to earn a higher profit. Investment gains hinge on an ongoing and long-term investment strategy that uses your risk tolerance and diversification to mitigate some risks. Even with these in place, you are exposing your money to loss. [5]

- When moving funds into a Rollover IRA, it’s important to understand the difference between a direct rollover and a 60-day rollover. In a direct rollover, the money moves from your employer plan straight into your Rollover IRA without you taking possession of the funds. No taxes are withheld, and the rollover is not considered taxable. In a 60-day rollover, the plan sends the funds to you directly, and you must deposit the full amount into your IRA within 60 days to avoid taxation. Employer plans are required to withhold 20% for federal taxes on 60-day rollovers, which you must replace out of pocket to avoid the withheld amount being treated as a taxable distribution. Because of this, most people choose direct rollovers when moving funds into a Rollover IRA. [12]

- Rollover IRAs are not limited in how many employer plan rollovers (such as from a 401(k), 403(b), or 457 plan) you can complete in a year. However, the IRS does impose a one-per-year rule on IRA-to-IRA 60-day rollovers. This restriction does not apply to direct rollovers or trustee-to-trustee transfers and does not apply when moving funds from an employer plan into a Rollover IRA. Most investors avoid 60-day rollovers altogether due to the withholding and timing requirements. Understanding this distinction helps you avoid accidental tax consequences and penalties that can result from using the wrong rollover method.[12]

- You can add personal money to these accounts, which might affect how it can be rolled into a new employer plan. 2,[7]

- Investment options include individual stocks, mutual funds, ETFs, annuities, UITs, etc. Investment vehicles not allowed in IRAs are Life Insurance, types of Derivatives Positions, antiques/collectibles, personal real estate, and most coins. [8]

- Fees vary from institution to institution. It is crucial to understand how much you are paying in fees.

- Investment control is either by your chosen institution or advisor or can be self-directed. With this type of account, you must know your risk tolerance and diversification strategy. These are especially important if you are self-directed and need to make changes to your investments as you make changes to your life and risk tolerance.[9]

- The earliest you can take penalty-free withdrawals is 59 ½. However, there are some exemptions to the early withdrawal penalty- if you are permanently and totally disabled, if you have medical expenses that exceed 10% of your modified adjusted gross income, the cost for your medical insurance while you’re unemployed, your qualified higher education expenses, the amount to buy, build or rebuild a first home (up to $10,000), your withdrawal is in the form of an annuity, your withdrawal is a qualified reservist distribution, you’re the beneficiary of a deceased IRA owner or the withdrawal is the result of an IRS levy.[10]

Traditional IRA: SECURE Act 2.0 Required Minimum Distribution (RMD) Ages

Traditional IRAs must follow the federal RMD schedule established under the SECURE Act 2.0. The age at which RMDs begin is based on your birth year:

RMD Age by Birth Year

-

Born before July 1, 1949 → Age 70½

-

Born July 1, 1949 through 1950 → Age 72

-

Born 1951–1958 → Age 73

-

Born 1960 or later → Age 75

-

Born 1959 → Pending IRS clarification

(A technical drafting error in SECURE 2.0 created an overlap between ages 73 and 75. The IRS is expected to issue final guidance.)

- You can convert funds from a Rollover IRA to a Traditional IRA because it is essentially a Traditional Account. You can convert these funds to a Roth IRA, but you will owe taxes on the converted money. However, the Roth funds will not be taxed at distribution, and Roth IRAs don’t have RMDs.[12],[13]

- Unlike employer-sponsored plans, Rollover IRAs do not allow loans. If you take a loan from your 401(k) and then leave your job, the outstanding balance is generally treated as a distribution unless repaid. Once funds are rolled into a Rollover IRA, loans are prohibited, and any withdrawal that is not an eligible distribution may be taxable and subject to penalties if you are under age 59½. Because IRAs cannot issue loans, rolling funds out of a workplace plan removes access to any future loan features the plan may have provided. [16]

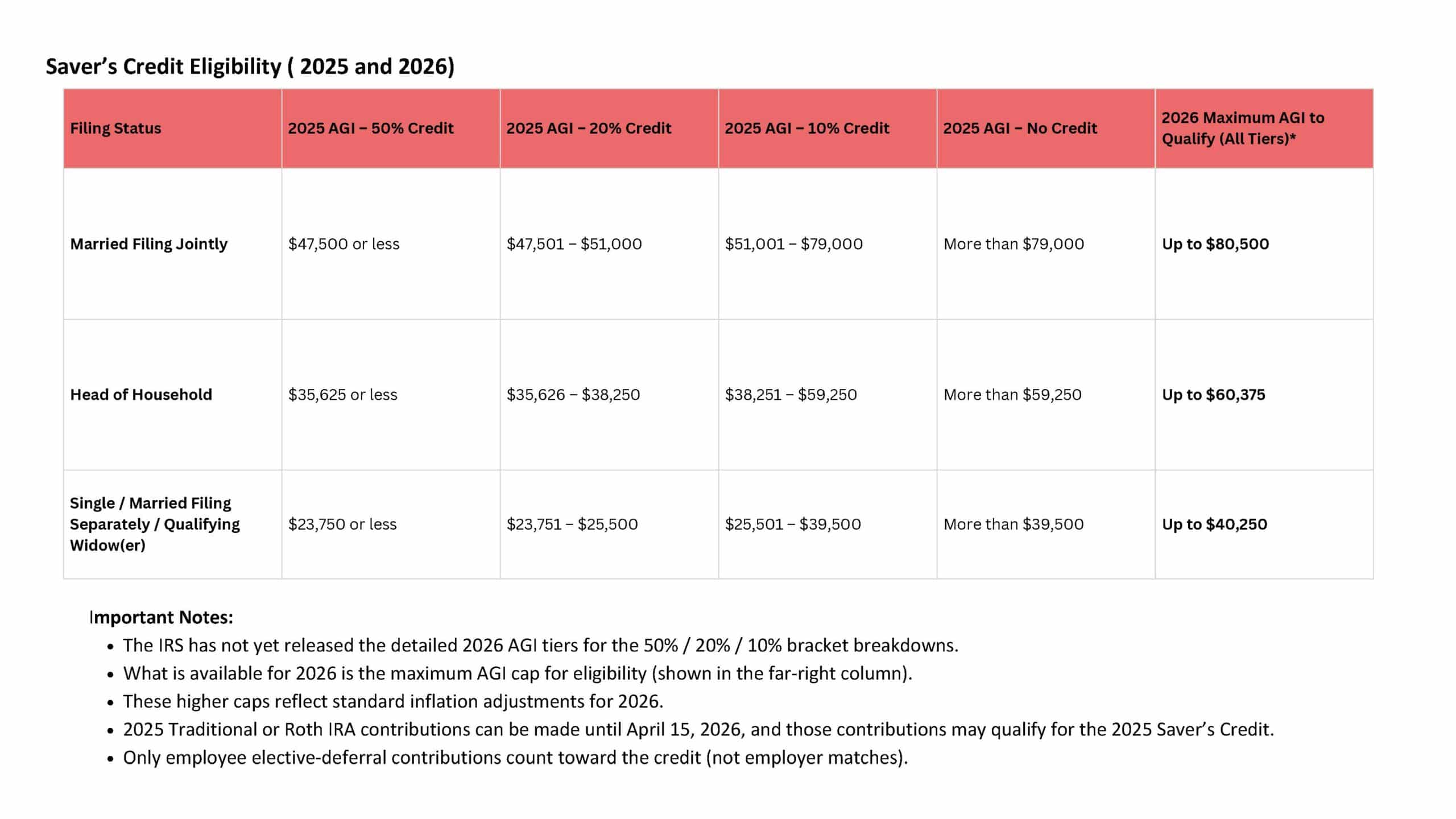

Saver’s Credit (Retirement Savings Contributions Credit)

The Saver’s Credit provides a tax benefit for contributing to eligible retirement accounts, helping lower- and moderate-income earners boost their long-term savings.

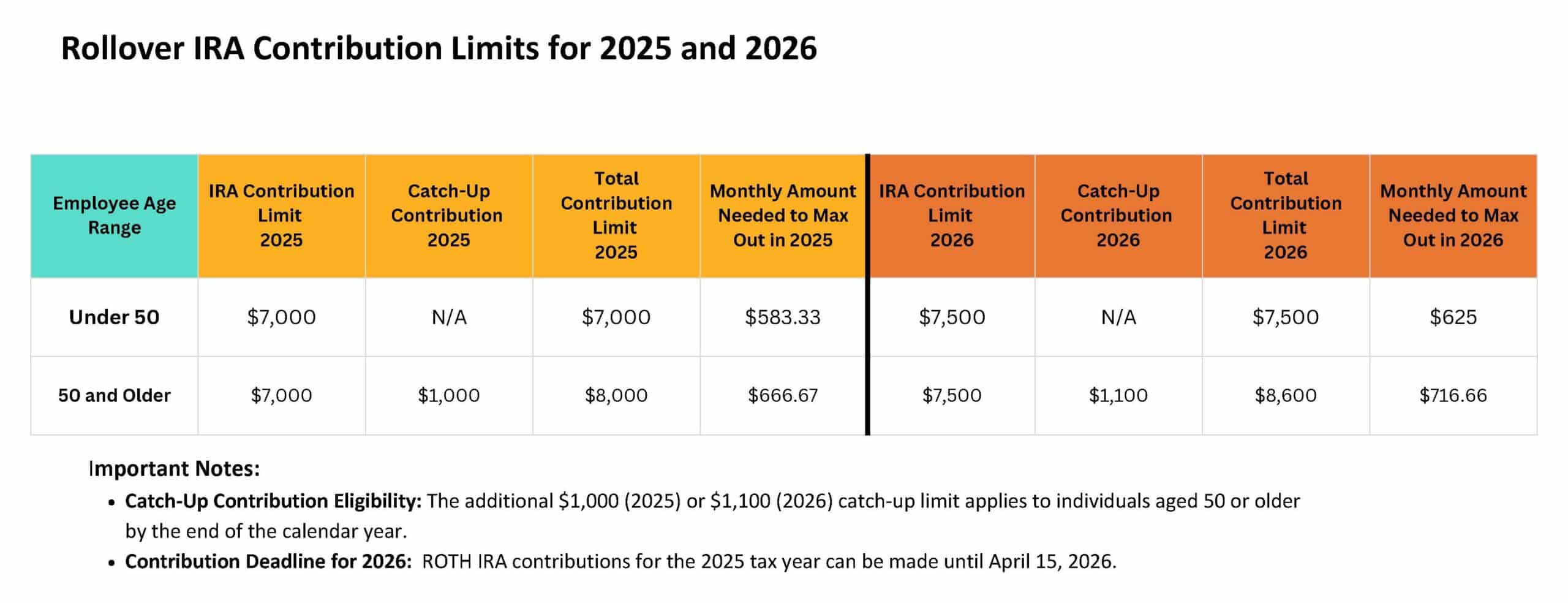

- If you have a Rollover IRA, Traditional IRA, and a Roth IRA, your total contribution limits for all accounts are $7,000 per year for those under age 50 and $8,000 for those 50 and older.

- There are no income limits to opening and contributing to a Rollover IRA.[15]

We want to help you explore additional retirement investment accounts that could work for your goals. Scarlet Oak Financial Services can be reached at 800.871.1219, or you can contact us here. To sign up for our newsletter with the latest economic news, click here.

Sources:

[1] https://www.sofi.com/learn/content/rollover-ira-vs-traditional-ira/

[2] https://obliviousinvestor.com/what-is-a-rollover-ira/

[3] https://www.investopedia.com/ask/answers/081915/my-ira-protected-bankruptcy.asp

[4] https://www.nerdwallet.com/article/investing/ira/what-is-a-traditional-ira

[5] https://www.investor.gov/sites/investorgov/files/2019-02/Saving-and-Investing.pdf

[6] https://www.irs.gov/newsroom/401k-limit-increases-to-23000-for-2024-ira-limit-rises-to-7000

[7] https://www.irs.gov/newsroom/401k-limit-increases-to-22500-for-2023-ira-limit-rises-to-6500#:~:text=Highlights%20of%20changes%20for%202023,to%20%246%2C500%2C%20up%20from%20%246%2C000.

[8] https://www.investopedia.com/articles/retirement/11/impermissable-retirement-investments.asp

[9] https://www.nerdwallet.com/article/investing/ira/what-is-a-traditional-ira

[10] https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-tax-on-early-distributions

[11] https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-required-minimum-distributions-rmds

[12] https://www.irs.gov/pub/irs-tege/rollover_chart.pdf

[13] https://www.investopedia.com/roth-ira-conversion-rules-4770480

[14] https://www.irs.gov/newsroom/401k-limit-increases-to-23000-for-2024-ira-limit-rises-to-7000

[15] https://www.investopedia.com/ask/answers/03/081503.asp

[16] https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-loans

https://www.irs.gov/newsroom/401k-limit-increases-to-23500-for-2025-ira-limit-remains-7000

https://www.irs.gov/pub/irs-drop/n-25-67.pdf

This material has been prepared for informational purposes. *To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on individual circumstances.