Introduction

Adjustable life insurance is a unique type of permanent, cash value policy designed for people who want both long-term protection and the ability to adapt their coverage as life changes. It blends the guarantees of whole life insurance with some of the flexibility found in universal life policies, allowing you to request changes to your premiums, death benefit, and cash value at certain intervals. This means you can structure your policy to meet your needs today and adjust it later as your circumstances evolve. Whether you are experiencing a major life event, navigating changes in income, or planning for long-term financial goals, adjustable life insurance can provide a balance of stability and adaptability.

What is it?

Permanent cash value policy combining features of whole life and universal life insurance

Adjustable life insurance is a type of permanent, cash value life insurance that combines features of both whole life and universal life insurance policies. This type of policy provides guarantees of death benefit and cash value, just as you would get with a whole life policy. What makes the adjustable life policy special is that, at specific intervals, the policy allows you to request upward or downward adjustments of the premiums, death benefit (face amount), or cash value, much like in a universal life policy. Increases in the death benefit above a certain amount usually require medical proof of insurability.

When can it be used?

You want a life insurance policy that can meet changing needs

Adjustable life insurance allows you to request changes to your premium, death benefit, and/or cash value, providing you with insurance coverage that can keep pace with your changing needs. You can structure your policy to resemble low-premium term life or high-premium limited pay whole life, and you can make changes later without having to buy additional policies. Policy changes are often requested at the time of family events, such as a child entering private school or college, the primary breadwinner’s loss of employment, or the start-up or failure of a business. The most common adjustment requested is a reduction of premium during a family’s period of decreased income or increased expenses.

You want some guarantees with your flexibility

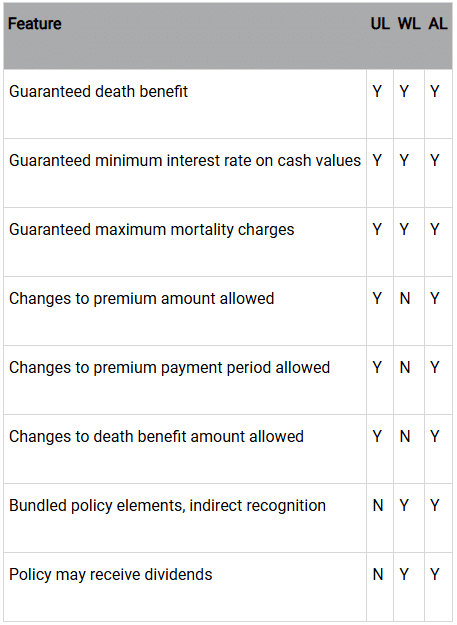

Adjustable life (AL) combines guarantees found in ordinary level premium whole life (WL) policies with some of the flexibility found in universal life (UL) policies, as shown in the following table:

Strengths

Provides benefits common to all cash value life insurance

Like all other permanent, cash value policies, an adjustable life policy contains the following features:

- Cash value grows tax deferred

- Cash value can be borrowed against (policy loans and withdrawals may reduce the policy’s cash value and death benefit)

You can change your premium amount and payment schedule

With an adjustable life policy, you are generally allowed (within limits) to request an increase or decrease of your premium amount or to lengthen or shorten the protection period (for instance, from term to whole life) and/or the premium payment period (for instance, from whole life to limited pay). When you make a change to your policy, it remains fixed until another change (if any) is requested. A formal adjustment agreement between you and the insurance company will probably be required.

You can change your death benefit

With adjustable life, you are allowed to change the death benefit (face amount) of your policy. Decreases to the death benefit may be permitted at any time, while increases may require evidence of insurability.

Tradeoffs

Adjustments may be allowed only at certain intervals and require advance notice

Although you are permitted to make changes to your adjustable life policy, generally the changes are allowed only at certain intervals and must be requested in advance. Once you make a change to your policy, it remains in effect until you make another formal change request.

Adjustment of premium payment or death benefit could lead to adverse tax consequences

The ability to increase the premium payments or reduce the death benefit has the potential to alter the policy so that it inadvertently becomes an MEC. Once classified as an MEC, the policy remains an MEC forever, and cash withdrawals, policy loans, and other transactions considered distributions under the contract could be subject to unfavorable income tax treatment and possibly penalties if taken before age 59½.

May be more expensive than other products when needs are known and unlikely to change

When your insurance needs are not likely to change and can be foreseen as relatively stable, there are other policy types that may prove to be more cost-effective. While the features of adjustable life can be very valuable when needed, there probably isn’t much value to paying for them when you don’t need them.

How to do it

Determine your life insurance need and overall financial goals

Before you buy life insurance, you need to know how much insurance you need. Insurance need is based on numerous factors, including your current age and income, marital status, number of incomes in the household, number of dependents, long-term financial goals, level of outstanding debt, and existing insurance and other assets. Your overall financial, estate, and tax-planning goals and your planning horizon should be considered as part of your insurance need evaluation.

Complete the insurance application and name your beneficiary

Before the insurance company can issue your policy, it must receive a completed application form. The application includes general health questions, and the process may include a physical examination, which is usually paid for by the insurance company. A critical part of the application is the beneficiary designation, or the naming of the person or persons to receive the policy proceeds when you die. Unless you make an irrevocable beneficiary designation, you can change the beneficiary designation by adding or removing a beneficiary or changing the percentages of the proceeds distribution.

Buy the policy and pay your premium

It is all well and good to know how much insurance and what type of policy is appropriate for your particular situation. But if you don’t actually buy the policy, you haven’t accomplished your goal! Not only that, but insurance becomes more expensive with age, so you won’t be doing your wallet any favors by delaying. An additional risk of delaying is that your health could change adversely. In other words, just because you are healthy and insurable today doesn’t mean you will be that way later. Deterioration in your health can mean higher premiums or an insurer considering you to be uninsurable.

Review your insurance need periodically and change your policy when needed

The amount of life insurance you need may change over time and with the occurrence of lifetime events. As a result, you should periodically review your life insurance coverage. As a rule, you should review your coverage every three years. Major lifetime events (such as the purchase of a home, birth or adoption of a child, and change in marital status) are also appropriate times to review your coverage. Reviewing your coverage will alert you to changes you may want or need in your policy (such as an increase in the death benefit) and help you prevent the mistake you can’t fix after you die: not having enough life insurance.

Tax considerations

Income Tax

Premium payments not deductible

Life insurance premium payments are generally not tax-deductible expenses.

Policy loan proceeds generally not taxable

When you take out a loan against your life insurance policy (except a policy classified as an MEC), the amount you receive is not considered taxable income. This rule applies even when the loan is larger than the amount of premiums you have paid in.

Policy loan interest not deductible

Interest you pay on a policy loan is not a tax-deductible expense when the loan is for purposes other than business or investments.

Policy cancellation may be taxable

If you cancel (surrender) your policy for cash, the gain on the policy is subject to federal income tax. The gain on a canceled policy is the difference between the net cash value and loan forgiveness amounts and your policy basis.

Policy lapse may be taxable

If you allow your policy to lapse, you could be subject to income tax even if you don’t receive any cash from the policy. A policy lapse can occur when you stop paying premiums and don’t have cash values available that can be used to pay the premiums. If you have an outstanding policy loan, it is possible you could be subject to tax on the amount of the loan plus any accrued but unpaid interest.

Death benefits generally not subject to federal income tax

Policy death benefits are generally not subject to federal income tax. One notable exception is when the policy has been sold or otherwise transferred for valuable consideration by one policyowner to another, subjecting it to the transfer-for-value rule.

Gift and Estate Tax

Policy proceeds not considered gift to beneficiary

When the proceeds of your life insurance policy are paid to a beneficiary, they are not treated as a gift for gift tax purposes. However, the insurance proceeds are generally included in your gross estate and will be subject to estate tax if they are.

Policy premium payments generally not subject to gift tax

When you are the owner of a policy on your own life, with another party as the beneficiary, premium payments made by you are not considered a gift to the beneficiary for gift tax purposes. If, however, someone else pays the premiums on a policy you own, the premium payments are considered a gift to you and may be subject to gift tax. Policy premiums generally qualify for the annual gift tax exclusion.

Policy proceeds included in estate value in most cases

The proceeds of a life insurance policy are included in the value of your estate if you held any incidents of ownership at any time during the three years before your death or if the proceeds are payable to you or your estate or executor. Incidents of ownership include (but are not limited to) the right to change the beneficiary, take out policy loans, or surrender the policy for cash.

Policy proceeds often exempt from state inheritance tax

In many states, life insurance proceeds are exempt from state inheritance taxes. Consult the laws of your state regarding tax treatment of life insurance proceeds.

Questions & Answers

How is adjustable life different from universal life?

Both adjustable life and universal life are permanent, cash value life insurance policies that provide you with the flexibility to change the premiums, face amount, and protection period. Adjustable life was available before universal life was developed. While the two policy types share similarities, there are fundamental differences in how the policy elements are recognized and how interest is credited to the cash value accounts. With adjustable life, the policy elements are bundled; in other words, the mortality and expense charges are not explicitly shown. Universal life contains unbundled policy elements, providing full disclosure of the individual charges for protection, expenses, and cash value. Another major difference between the two types of policy is that you must formally request policy changes in advance with adjustable life. Changes to universal life policies can happen without prior notice to the insurance company, but the privilege is reflected in the policy premiums.

Conclusion

Adjustable life insurance can be an excellent option for those who want lifelong coverage with the ability to make changes over time. It offers valuable flexibility to adjust premiums and benefits as your needs change while maintaining the foundational guarantees of a permanent policy. However, making adjustments can have tax and cost implications, and the policy may be more expensive than other options if your needs remain stable. Because of the complexities involved, it is essential to review your policy regularly and work with a financial or insurance professional to ensure that any changes align with your overall financial goals. Taking the time to structure and maintain the right policy can provide lasting protection for your loved ones and peace of mind for you.

Scarlet Oak Financial Services can be reached at 800.871.1219 or contact us here. Click here to sign up for our newsletter with the latest economic news.

Source:

Broadridge Investor Communication Solutions, Inc. prepared this material for use by Scarlet Oak Financial Services.

Broadridge Investor Communication Solutions, Inc. does not provide investment, tax, legal, or retirement advice or recommendations. The information presented here is not specific to any individual’s personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on individual circumstances. Scarlet Oak Financial Services provide these materials for general information and educational purposes based upon publicly available information from sources believed to be reliable — we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.