Here are some notable changes affecting individual taxpayers this year (the changes are far less seismic in 2019 than those brought about in 2018 by the Tax Cuts & Jobs Act).

Just a reminder as you move to this new section on Tax Changes & COLAs for Households. This guide is not intended to provide tax or legal advice. Be sure to consult with a qualified tax or financial professional before making short-term or long-term changes to your tax or financial strategy.

1) Income tax brackets have been adjusted for inflation.

The I.R.S. has made some 2019 cost-of-living adjustments, or COLAs, resulting in slightly altered taxable income thresholds:

2) The standard deduction has increased a bit.

Another COLA here. The increase ranges from $200-$400, depending on filing status.

- Single filer: $12,200 (instead of $12,000)

- Married couples filing separately: $12,200 (instead of $12,000)

- Head of household: $18,350 (instead of $18,000)

- Married couples filing jointly & surviving spouses: $24,400 (instead of $24,000)

The additional standard deduction is $1,300 this year for single filers who are blind or aged 65 or older (and $1,650 for unmarried taxpayers blind or aged 65 or older). A person who is claimed as a dependent on another taxpayer’s 1040 form for 2019 can take a standard deduction of either a) $1,100 or b) the sum of $350 + that person’s earned income, whichever is greater.7

3) AMT exemption amounts have also received a COLA.

The Tax Cuts & Jobs Act made the exemption amounts for the Alternative Minimum Tax permanently subject to inflation indexing. Here are the inflation-adjusted exemption amounts for 2019.

- Single filer or head of household: $71,700

- Married couples filing separately: $55,850

- Married couples filing jointly & surviving spouses: $111,700

- Trusts and estates: $25,000

How about the thresholds where these exemptions begin to phase out? For 2019, they are set now at $510,300 for individuals and $1,026,000 for joint filers.7,8

4)The Affordable Care Act penalty for not having health insurance has been cut to $0.

Technically, the penalty linked to the ACA individual mandate is not “gone” – but it is suspended for 2019, and perhaps, years to come. This development does not necessarily mean that if you go without health insurance, you will face no penalty this year. In some states (such as New Jersey), legislatures are considering or approving bills to impose state fines on uninsured taxpayers.

The other provisions and stipulations of the ACA remain in place, including the employer shared responsibility provision and the requirement for self-insured employers to report worker coverage using Form 1095-C or Form 1095-B.9

5) The AGI threshold for the qualified medical expense deduction has risen.

This itemized deduction provides a significant tax break for some households. It permits a taxpayer to deduct out-of-pocket medical (and dental) expenses exceeding a percentage of adjusted gross income (AGI). For 2018, the percentage threshold was set at 7.5% of AGI. This year, it climbs to 10%, meaning this deduction will be reduced.7

6) The federal tax treatment of alimony payments has changed.

Should you happen to divorce this year, any alimony paid to you in the wake of a divorce finalized on or after January 1, 2019 will be considered tax-exempt income. That is a change from 2018 and before, when alimony received was defined as taxable income.

Before 2019, alimony payments made from a higher-earning ex-spouse to a lower-earning ex-spouse were tax deductible. Now, that is no longer the case, unless the payments result from a divorce finalized before January 1, 2019.10

7) Contribution limits on many retirement plans have increased this year.

For Roth and traditional IRAs, the annual contribution limit is now $6,000 (rising by $500 in 2019, the first increase in six years), with the usual $1,000 “catch-up” contribution allowed for IRA owners 50 and older. Roth IRA contributions cannot be made by taxpayers with high incomes. To qualify for the tax-free and penalty-free withdrawal of earnings, Roth IRA distributions must meet a five-year holding requirement and occur after age 59½. Tax-free and penalty-free withdrawal also can be taken under certain other circumstances, such as a result of the owner’s death. The original Roth IRA owner is not required to take minimum annual withdrawals.11

Withdrawals from traditional IRAs are taxed as ordinary income and, if taken before age 591/2, may be subject to a 10% federal income tax penalty. Generally, once you reach age 70 1/2, you must begin taking required minimum distributions.11

For employer-sponsored retirement plans such as 401(k)s, 403(b)s, most 457 plans, and the federal government’s Thrift Savings Plan (TSPs), the annual contribution cap is now $500 higher at $19,000, with the “catch-up” contribution permitted for plan participants 50 and older remaining at $6,000. Distributions from 401(k) plans and most other employer-sponsored retirement plans are taxed as ordinary income and, if taken before age 59½, may be subject to a 10% federal income tax penalty. Generally, once you reach age 70½, you must begin taking required minimum distributions.11

TSP follow the same contribution guidelines as 401(k)s. However, the total amount a TSP member can contribute in any given year is up to $54,000 under the Maximum Annual Addition Limit11

Yearly contribution limits for SIMPLE retirement accounts also rise by $500 for 2019, to $13,000. The annual catch-up contribution limit for older plan participants is unchanged at $3,000. Distributions for SIMPLE-IRAs and solo 401(k) are taxed as ordinary income and, if taken before age 59½, may be subject to a 10% federal income tax penalty. The penalty may be as much as 25% if a withdraw is taken the first two years of plan participation. A SIMPLE-IRA is only available to businesses with 100 or fewer employees who earned at least $5,000 in the prior year. To use a SIMPLE-IRA, a business cannot offer any other employer-sponsored retirement plan.11

Self-employed individuals and small business owners may direct employer contributions (as a percentage of salary) of up to $56,000 this year into SEP-IRAs and solo 401(k)s, up from $55,000 in 2018. That is the new annual limit for the amount of money that can be directed into defined contribution plans in 2019. (The annual compensation limit that figures into the savings calculation for such plans increases from $275,000 to $280,000.) Distributions from SEP-IRAs are taxed as ordinary income and, if taken before age 59½, may be subject to a 10% federal income tax penalty. Generally, once you reach age 70½, you must begin taking required minimum distributions. IRAs have exceptions to avoid the 10% withdrawal penalty, including death and disability. Unlike the self-employed 401(k), which is only available to business owners with no employees, you cannot take a loan from your SEP assets11,12

The maximum amount that a defined benefit plan may pay a participant each year rises $5,000 to $225,000 in 2019.11

Are you a business owner whose company has an employee stock ownership plan, or ESOP? You should know that the dollar amount for figuring the maximum account balance in an ESOP subject to a 5-year distribution period is now $1.13 million. The dollar amount used to determine the lengthening of that period is now $225,000.12

In addition to these COLAs:

*Another 2019 COLA affects the definition of a key employee who participates in a top-heavy workplace retirement plan. That cap rises $5,000 this year, to $180,000.

*Similarly, the dollar threshold for the definition of a highly compensated employee in a 401(k) plan heads north by $5,000 to $125,000.12

8) Phase-out ranges affecting Roth and traditional IRA contributions have been altered for 2019.

*Traditional IRA Contribution Deductions When You or Your Spouse Has Access to a Retirement Plan at Work

In 2019, the modified adjusted gross income (MAGI) phase-out ranges are:

*Single filer or head of household: $64,000 – $74,000 ($1,000 higher)

*Married couples filing jointly: $103,000 – $123,000 ($2,000 higher)

*Married couples filing separately: $0 – $10,000 (it never changes)

If your MAGI falls below these phase-out ranges, contributions to a traditional IRA are fully deductible.12

*Traditional IRA Contributions if You Lack Access to a Workplace Retirement Plan, but Your Spouse Has Access to Such a Plan

*Married couples filing jointly: $193,000 – $203,000 ($4,000 higher)

*Married couples filing separately: $0 – $10,000 (it never changes)12

*Roth IRA Contributions

Your ability to make a 2019 Roth IRA contribution is reduced when your MAGI falls into these phase-out ranges. Beyond the high end of these ranges, that ability disappears.

*Single filer or head of household: $122,000 – $137,000 ($2,000 higher)

*Married couples filing jointly: $193,000 – $203,000 ($4,000 higher)

*Married couples filing separately: $0 – $10,000 (it never changes)12

9) The federal estate and gift tax exemption has also had a COLA.

In 2019, it rises to $11.4 million for individuals, up from the previous $11.2 million. An ultra-wealthy married couple now has a chance to protect up to $22.8 million of their estate from federal death taxes (which can reach 40%), provided the surviving spouse elects to use the late spouse’s unused portion of their estate and gift tax exemption. (According to the Tax Policy Center, less than 2,000 estates were subject to federal death taxes in 2018.)13

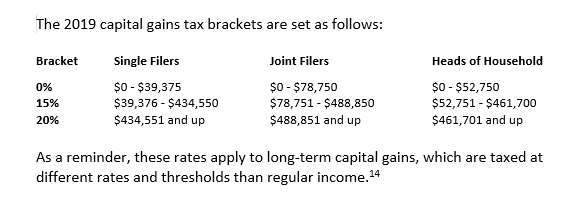

10) Capital gains tax thresholds have been adjusted slightly northward this year.

The 2019 capital gains tax brackets are set as follows:

11) You can earn slightly more and claim the Saver’s Credit.

The yearly MAGI limit for this tax credit, an incentive to foster greater retirement savings among low-income and moderate-income workers, has risen as follows:

*Single filers and married couples filing separately: $32,000 ($500 higher)

*Head of household: $48,000 ($750 higher)

*Married couples filing jointly: $64,000 ($1,000 higher)12

12) The maximum Earned Income Tax Credit (EITC) has been adjusted for 2019.

This year, the maximum EITC is $6,557 for taxpayers with three or more qualifying children, $5,828 for taxpayers with two or more qualifying children, $3,526 for taxpayers with one qualifying child, and $529 for taxpayers without any qualifying children. These amounts have increased a bit from 2018.14

13) Another COLA concerns the phaseout thresholds for the Lifetime Learning Credit.

This education credit can be as large as $2,000 (that is, the credit can be equal to 20% of the first $10,000 you spend on qualified higher education expenses in 2019). The MAGI phase-out range for single filers and heads of household is $58,001 – $68,000. For joint filers, it is $116,000 – $134,000. Above the high ends of these phase-out ranges, you cannot claim the credit.15

14) Some COLAs apply to the Adoption Credit.

In 2019, the MAGI phase-out range for this tax credit is $211,161 – $251,160; above $251,160, the credit cannot be claimed. The credit maxes out at $14,080 of qualified adoption expenses for a child with special needs this year and $13,810 of qualified adoption expenses for other adoptions.7,16

15) More COLAs apply to Health Savings Accounts and Medical Savings Accounts.

In 2019, the yearly individual and family contribution caps for HSAs are, respectively, $50 and $100 higher, at $3,500 and $7,000. (An additional catch-up contribution of up to $1,000 is permitted for accountholders 55 and older.) As for the high-deductible health plan (HDHP) requirements, the minimum deductible has not changed for 2019 (at least $1,350 for individuals; at least $2,700 for families); the annual out-of-pocket expense limit has risen $100 for individuals, to $6,750, and increased $200 for families, to $13,500.

For MSAs, the criteria for linked HDHPs has changed slightly. The linked HDHP must have a yearly deductible between $2,350-$3,500 for an individual and between $4,650-$7,000 for a family. The maximum out-of-pocket expenses for an individual this year: $4,650. For family coverage: $8,550.5,7

16)The hardship withdrawal rules for 401(k)s have changed.

The Bipartisan Budget Act of 2018 brought some changes following in the path of the Tax Cuts and Jobs Act of 2017. There are three changes to note this year, and they also apply to similar retirement plans in the nonprofit sector.

*Qualified non-elective contributions, qualified matching contributions, and account earnings may all be taken as part of hardship withdrawals from 401(k) plans.

*A 401(k) plan participant may now take a hardship withdrawal without having to take a loan from the plan first.

*Participants in 401(k)s no longer need to wait six months to resume contributing to a plan after taking a hardship withdrawal.

Of course, not all employer-sponsored retirement plans allow hardship withdrawals; those that do allow them are being directed to follow these new rules and amend plan documents.17

17) There are higher limits on the foreign earned income exclusion.

If you earn income while living and working in another country in 2019, and you are eligible to claim the foreign earned income exclusion, you may shield up to $105,900 of such earned income this year. For 2018, the limit was $103,900.7

This Special Report is not intended as a guide for the preparation of tax returns. The information contained herein is general in nature and is not intended to be, and should not be construed as, legal, accounting or tax advice or opinion. No information herein was intended or written to be used by readers for the purpose of avoiding penalties that may be imposed under the Internal Revenue Code or applicable state or local tax law provisions. Readers are cautioned that this material may not be applicable to, or suitable for, their specific circumstances or needs, and may require consideration of non-tax and other tax factors if any action is to be contemplated. Readers are encouraged to consult with professional advisors for advice concerning specific matters before making any decision. Both Scarlet Oak Financial Services/ Faye Sykes and MarketingPro, Inc. disclaim any responsibility for positions taken by taxpayers in their individual cases or for any misunderstanding on the part of readers. Neither Scarlet Oak Financial Services, Faye Sykes, nor MarketingPro, Inc. assume any obligation to inform readers of any changes in tax laws or other factors that could affect the information contained herein.

This material was prepared by MarketingPro, Inc. for use by Scarlet Oak Financial Services and Faye Sykes.

Citations.

1 – cnbc.com/2019/01/08/irs-confirms-tax-season-to-start-jan-28-despite-government-shutdown.html [1/8/19]

2 – blog.indinero.com/2019-business-tax-deadlines [6/1/18]

3 – thebalancesmb.com/payroll-tax-deadlines-for-january-and-february-3974577 [1/4/19]

4 – taxact.com/support/24459/2018/irs-filing-deadlines [1/10/19]

5 – trustetc.com/resources/investor-awareness/contribution-limits [11/1/18]

6 – shrm.org/resourcesandtools/hr-topics/benefits/pages/agencies-preview-form-5500-for-2019-filings-while-revamp-delayed.aspx [11/26/18]

7 – forbes.com/sites/kellyphillipserb/2018/11/15/irs-announces-2019-tax-rates-standard-deduction-amounts-and-more [11/15/18]

8 – fool.com/taxes/2018/12/15/your-2019-guide-to-the-alternative-minimum-tax.aspx [12/15/18]

9 – paychex.com/articles/compliance/aca-individual-mandate-penalty-reduced-2019 [12/21/18]

10 – foxbusiness.com/business-leaders/amazon-ceo-jeff-bezos-divorce-subject-to-these-tax-changes [1/10/19]

11 – forbes.com/sites/ashleaebeling/2018/11/01/irs-announces-2019-retirement-plan-contribution-limits-for-401ks-and-more/ [11/1/18]

12 – irs.gov/newsroom/401k-contribution-limit-increases-to-19000-for-2019-ira-limit-increases-to-6000 [11/27/18]

13 – forbes.com/sites/ashleaebeling/2018/11/15/irs-announces-higher-2019-estate-and-gift-tax-limits [11/15/18]

14 – taxfoundation.org/2019-tax-brackets [11/28/18]

15 – thebalance.com/lifetime-learning-tax-credit-3192933 [1/11/19]

16 – tinyurl.com/ycdgvpr5 [1/14/19]

17 – investrustwealthmanagement.com/2018/09/27/what-are-the-new-rules-for-401k-hardship-withdrawals/ [9/27/18]

18 – tax.thomsonreuters.com/news/moves-that-will-maximize-the-new-deduction-for-pass-through-income [12/12/18]

19 – shrm.org/resourcesandtools/hr-topics/compensation/pages/fica-social-security-tax-2019.aspx [12/19/18]

20 – irs.gov/pub/irs-pdf/p334.pdf [2019]

21 – tinyurl.com/ycd6bl8q [12/14/18]

22 – medicareresources.org/faqs/what-kind-of-medicare-benefit-changes-can-i-expect-this-year/ [10/15/18]

23 – forbes.com/sites/howardgleckman/2019/01/15/the-new-1040-will-fit-on-a-big-postcard-but-it-wont-make-tax-filing-any-simpler [1/15/19]