In 2021, the average cost of college in the United States is $35,720 per student per year. If that number grows at the same annual growth rate of 6.8% that it has for the last 20 years, that financial expense is just becoming more extensive. You want to help support your child’s college dreams but feel lost as to your best options for building a college fund that works for you and your family. These days most families need some sort of financial aid. Understanding what FASFA looks at as income and assets is crucial as you build your college savings plan.

Chart source: https://www.cappex.com/articles/money/how-to-shelter-assets-on-the-fafsa

Here are some key aspects of some college funds:

Custodial account UTMA (In Child’s Name)

- Children gain control at the age of maturity, dictated by your state (In Georgia, the age is 21).

- Money can be used only by the child on the account.

- Money can be spent for any of the child’s needs – cars, trips, tuition, phones, clothing, etc.

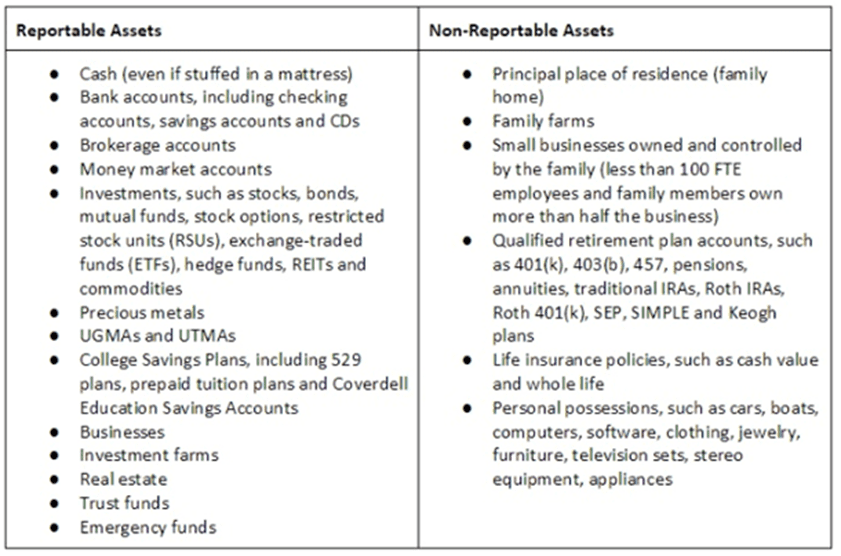

- This account is counted on FASFA for college aid and can limit financial aid.

- No contribution limits. Also, anyone can contribute to the fund, whether they are family or friends.

- Investment options are very flexible.

- This is income attributed to the child, and taxes are annually based on growth and dividends.

529 College plan (In Child’s Name)

- Parents control money, and one account can be used for multiple children.

- Anyone can contribute to the fund, whether they are family or friends.

- This account can only be used for school-related expenses. The fund could not be used for transportation or the purchase of a car.

- This account is counted on FASFA for college aid and can limit financial aid.

- Investment options are limited.

- There is a 10% penalty if not used for educational costs.

- There are incentives like tax deductions and matching contributions with some plans, but this varies with each state.

- If you open with TIAA Cref, the Georgia state plan, contributions are a state tax deduction. Click here for the Georgia 529 plan sign-up.

Whole life insurance (On Child)

- Parents control money as long as they want and are paying the premiums.

- Each child would need his or her own policy.

- This account is NOT counted on FASFA for college aid and will not be a reportable asset for financial aid.

- Whole life insurance builds cash value. As education expenses are accrued, you would pull from this.

- This type of early policy guarantees insurability for the child into adulthood.

- This policy can become part of your family’s estate and legacy planning.

Roth IRA (in parent’s names)

- Parents control the account. These post-tax accounts are primarily used for retirement, but they can be used for college funding because of the penalty exemption rule.

- A distribution for college expenses falls under the penalty exemption rules for IRS. The account needs to be open for at least five years to pull from this account and avoid the under 59 ½ 10% penalty.

- If this fund is also being used as a retirement fund, the parents will lose out on the earning potential of the used money.

- This account is NOT counted on FASFA for college aid and will not be a reportable asset for financial aid.

- In 2021, the yearly contribution limits are $6,000 per year for those under age 50. People 50 and older can make an additional $1,000 catch-up contribution.

- If withdrawals are beyond contribution total, there will be income tax on the earnings portion of the withdrawal.

A supplement to your college savings could be rewards programs like Upromise. Upromise has members open accounts that earn rewards with the use of the account. Those cash rewards can be transferred into a designated 529 College Savings Plan account or checking/savings account. Family and friends can sign up for a Upromise account that accumulates rewards to help with a college fund. Click here to read more about Upromise.

If you’d like to speak with us about college funding or any aspect of your financial life, Scarlet Oak Financial Services can be reached at 800.871.1219 or contact us here.

Sources:

https://www.morningstar.com/articles/920020/can-i-use-a-roth-ira-to-pay-for-college

https://www.fbfs.com/learning-center/the-5-education-withdrawal-rules-you-need-to-know

This material has been prepared for informational purposes.