In this week’s recap: Markets react to dim forecast, 2Q reports.

Weekly Economic Update

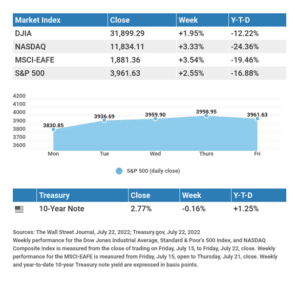

THE WEEK ON WALL STREET

Stocks rallied last week as investor spirits lifted thanks to a better-than-expected start to the second-quarter earnings season.

The Dow Jones Industrial Average gained 1.95%, while the Standard & Poor’s 500 added 2.55%. The Nasdaq Composite index jumped 3.33% for the week. The MSCI EAFE index, which tracks developed overseas stock markets, advanced 3.54%.1,2,3

EARNINGS PROPEL STOCKS

Earnings season kicked off last week, with major banks reporting second-quarter results. While their results were mixed, they appeared to indicate that consumers and businesses remained reasonably healthy–a perspective that helped erase some negative sentiment overhanging the market.

As the week progressed, stocks gained momentum as earnings results poured in from different sectors of the economy, showing that businesses were navigating higher inflation and slowing growth better than investors feared. Technology and other gloomier sectors were among the market’s best performers for the week. A few disappointing corporate reports and a weak economic report sent stocks lower to close out a solid week.

CRACKS IN THE FOUNDATION

Data released last week indicated more trouble in the housing market. The latest monthly homebuilder sentiment survey showed the single largest monthly drop in its 37-year history, except for April 2020. The sentiment report preceded a drop in June housing starts and issued building permits. Housing starts declined for the second month, falling 2.0% and surprising economists who had expected an increase. 4,5

Housing weakness made itself known through a 5.4% month-over-month decline in June’s existing home sales, representing the slowest pace since June 2020. Increasing prices and higher mortgage rates demonstrated drags on buyer demand. 6

THE WEEK AHEAD: KEY ECONOMIC DATA

THE WEEK AHEAD: KEY ECONOMIC DATA

- Tuesday: New Home Sales.

- Wednesday: FOMC Announcement. Durable Goods Orders.

- Thursday: Gross Domestic Product (GDP). Jobless Claims.

Source: Econoday, July 22, 2022

The Econoday economic calendar lists upcoming U.S. economic data releases (including key economic indicators), Federal Reserve policy meetings, and speaking engagements of Federal Reserve officials. The content is developed from sources believed to be providing accurate information. The forecasts or forward-looking statements are based on assumptions and may not materialize. The forecasts also are subject to revision.

THE WEEK AHEAD: COMPANIES REPORTING EARNINGS

- Tuesday: Microsoft Corporation (MSFT), General Electric Company (GE), Visa, Inc. (V), Alphabet, Inc. (GOOGL), General Motors Company (GM), The Coca Cola Company (KO), McDonald’s Corporation (MCD), Archer Daniels Midland Company (ADM), 3M Company (MMM), Texas Instruments, Inc. (TXN), United Parcel Service, Inc. (UPS), KimberlyClark Corporation (KMB).

- Wednesday: The Boeing Company (BA), Ford Motor Company (F), Qualcomm, Inc. (QCOM), Bristol Myers Squibb Company (BMY), Lam Research Corporation (LRCX), Shopify, Inc. (SHOP), ServiceNow, Inc. (NOW), General Dynamics Corporation (GD), Norfolk Southern Corporation (NSC).

- Thursday: Apple, Inc. (AAPL), Intel Corporation (INTC), Mastercard, Inc. (MA), Pfizer, Inc. (PFE), Merck & Co., Inc. (MRK), The Southern Company (SO), Northrop Grumman Corporation (NOC), Southwest Airlines (LUV).

- Friday: AbbVie, Inc. (ABBV), Exxon Mobil Corporation (XOM), Chevron Corporation (CVX), The Procter & Gamble Company (PG), ColgatePalmolive Company (CL).

Source: Zacks, July 22, 2022

Companies mentioned are for informational purposes only. It should not be considered a solicitation for the purchase or sale of the securities. Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The return and principal value of investments will fluctuate as market conditions change. When sold, investments may be worth more or less than their original cost. Companies may reschedule when they report earnings without notice.

Scarlet Oak Financial Services can be reached at 800.871.1219 or contact us here. Click here to sign up for our weekly newsletter with the latest economic news.

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The return and principal value of investments will fluctuate as market conditions change. When sold, investments may be worth more or less than their original cost.

The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice.

The market indexes discussed are unmanaged, and generally, considered representative of their respective markets. Index performance is not indicative of the past performance of a particular investment. Indexes do not incur management fees, costs, and expenses. Individuals cannot directly invest in unmanaged indexes. Past performance does not guarantee future results.

The Dow Jones Industrial Average is an unmanaged index that is generally considered representative of large-capitalization companies on the U.S. stock market. Nasdaq Composite is an index of the common stocks and similar securities listed on the NASDAQ stock market and is considered a broad indicator of the performance of technology and growth companies. The MSCI EAFE Index was created by Morgan Stanley Capital International (MSCI) and serves as a benchmark of the performance of major international equity markets, as represented by 21 major MSCI indexes from Europe, Australia, and Southeast Asia. The S&P 500 Composite Index is an unmanaged group of securities that are considered to be representative of the stock market in general.

U.S. Treasury Notes are guaranteed by the federal government as to the timely payment of principal and interest. However, if you sell a Treasury Note prior to maturity, it may be worth more or less than the original price paid. Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors.

International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets. These factors may result in greater share price volatility.

Please consult your financial professional for additional information.

This content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation. This material was developed and produced by FMG Suite to provide information on a topic that may be of interest. FMG is not affiliated with the named representative, financial professional, Registered Investment Advisor, Broker-Dealer, nor state- or SEC-registered investment advisory firm. The opinions expressed and material provided are for general information, and they should not be considered a solicitation for the purchase or sale of any security.

Copyright 2022 FMG Suite.

CITATIONS:

- The Wall Street Journal, July 22, 2022

- The Wall Street Journal, July 22, 2022

- The Wall Street Journal, July 22, 2022

- CNBC, July 18, 2022

- The Wall Street Journal, July 19, 2022

- CNBC, July 20, 2022