![Understanding Traditional 401(k) Plans [2026]](https://scarletoakfs.com/wp-content/uploads/2025/01/Understanding-Traditional-401k-Plans-2025.jpg)

Traditional 401(k) plans are the most widely offered employer-sponsored retirement programs in the private sector. They allow employees to save for retirement directly from their paychecks while receiving valuable tax benefits. These plans form the backbone of workplace retirement savings in the U.S., with millions of workers using them to accumulate long-term, tax-advantaged wealth.

Employers may also offer matching contributions, automatic enrollment features, and various investment options, making the 401(k) one of the most flexible and powerful retirement savings tools available. While plan features vary by employer, most 401(k)s offer tax-deferred growth, multiple investment choices, and clear eligibility rules that help employees build consistent retirement savings over time.

Key aspects of Traditional 401(k) plans:

- They are a pre-tax investment account, meaning the money you place in this account is deducted from your check before taxes are collected. For example, if your weekly check is $1000 and you contribute $50 to your 401(k) account, it will show you made $950 weekly on your annual tax return. That money accumulates in the account tax-free until you withdraw it.[1]

- With all investment accounts, you expose some or all your invested money to loss for the chance to earn a higher profit. Investment gains hinge on an ongoing and long-term investment strategy that uses your risk tolerance and diversification to mitigate some risks. Even with these in place, you are exposing your money to loss.[2]

- Any private or public company can have 401(k) funds if there are 20 or more employees.1

- Employers must allow all employees to participate if they are 21 and above, have one year of service, and have 1000 hours per year. There are some restrictions beyond this for people who are not US citizens and some types of union members.1

- 401(k) plans usually provide at least three investment choices, but some offer many more options. But, again, this will vary from company to company. This variation in options is good to ask about in the hiring process.[3]

![Understanding Traditional 401(k) Plans [2025]](https://scarletoakfs.com/wp-content/uploads/2025/01/401k-scaled.jpg)

Catch Up Groups:

Employees age 50 or older (the standard catch-up eligibility age). Enhanced catch-up limits apply separately for ages 60–63 beginning in 2025 under SECURE 2.0.

How the $145,000 Threshold Is Determined

Based on Box 3 Social Security wages from the prior calendar year, it applies separately by employer under controlled group rules.

- Beginning in 2025, long-term, part-time employees who have completed at least 500 hours of service annually for three consecutive years will be eligible to participate in their employer’s 401(k) plan.

- Enacted in 2025, newly established 401(k) and 403(b) plans are generally required to automatically enroll eligible employees, with an initial deferral rate of at least 3% of compensation. Eligible employees must be auto-enrolled at a 3% minimum contribution rate, increasing annually by 1% until reaching 10-15%. This applies to plans established after December 29, 2022, excluding new/small businesses, church, and government plans.

- The average match for most companies in 2023 was 5%.[9] The amount and ways matching is created in a 401k plan widely varies, but the total contribution between employer and employee cannot exceed defined limits in the chart below. In addition, matching cannot make up more than 25% of compensation for an employee. [10],[11]

Automatic Rollover Threshold: Previously, if a former employee’s 401(k) balance was less than $5,000, plan administrators could transfer the funds into an IRA without the employee’s consent. The SECURE 2.0 Act raised this limit to $7,000, effective from 2025.

- Vesting is when you must stay with an employer to keep any money they match. The vesting period varies with employers but usually is in the range of 3 to 6 years. There are also variations in vesting schedules. Cliff vesting is where you go 100% vested at a set period. Graded vesting is where you earn a percentage of 100% each year. An example would be you are 33% vested in year one, 66% in year two, and 100% in year three.[12]

- A 401(k)-plan sponsor is the plan fiduciary, legally responsible for selecting the plan’s investment options and monitoring their suitability. Generally, your employer is your 401(k)-plan sponsor.[13]

- If you leave an employer, you can take your money with you.[14]

- Employee deferral limit (e.g., $24,500 in 2026) applies across ALL jobs combined — but employer contributions are separate.

Simplified Hardship Withdrawals: The SECURE 2.0 Act allows for self-certification of hardship withdrawals, simplifying the process for participants to access funds in case of financial emergencies.

- 401(k)s are required to perform nondiscrimination tests (NDTs) annually to ensure that 401(k) retirement plans benefit all employees, not just high earners or company owners.[15]

- Fees vary from plan to plan, but the three categories are investment fees, plan administration fees, and individual service fees. It is crucial to understand how much you are paying in fees.[16]

- The earliest you can take penalty-free withdrawals is 59 ½, and the penalty is an extra 10% on top of the taxes collected. However, there are some exemptions to the early withdrawal penalty- if you are permanently and totally disabled, if you lose your job at 55 or older, if you have medical expenses that exceed 10% of your modified adjusted gross income, with some divorce settlement types and if you die.8

Secure Act 2.0: Required Minimum Distribution (RMD) Age for Traditional 401(k) Accounts

Traditional 401(k) accounts must follow the federal RMD schedule established under the SECURE Act and SECURE 2.0. The age at which RMDs begin depends on your birth year:

-

Born before 7/1/1949 → RMD age 70½

-

Born 7/1/1949–1950 → RMD age 72

-

Born 1951–1958 → RMD age 73

-

Born 1960 or later → RMD age 75

-

Born in 1959 → Federal clarification pending (age 73 or 75)

RMDs apply to Traditional 401(k) balances regardless of employment status after retirement. If you continue working past RMD age and continue contributing to your employer’s 401(k), some plans allow those new contributions to offset or reduce that year’s RMD, depending on how the plan administrator applies the calculation. This varies by plan and should be confirmed with the employer or plan provider. [17],[18]

- You can take a low-interest loan on 401(k) accounts, up to $50,000 or 50% of your account balance. Still, you will have to pay it back sometimes within 90 days but definitely within five years (this period may be extended if the money is used to buy a primary home) or at leaving that job, or it becomes taxable income. The payments will most likely be held back from your paycheck. Some plans don’t let you contribute to your account until the loan is paid back. Interest charges go directly back into your retirement account.[19]

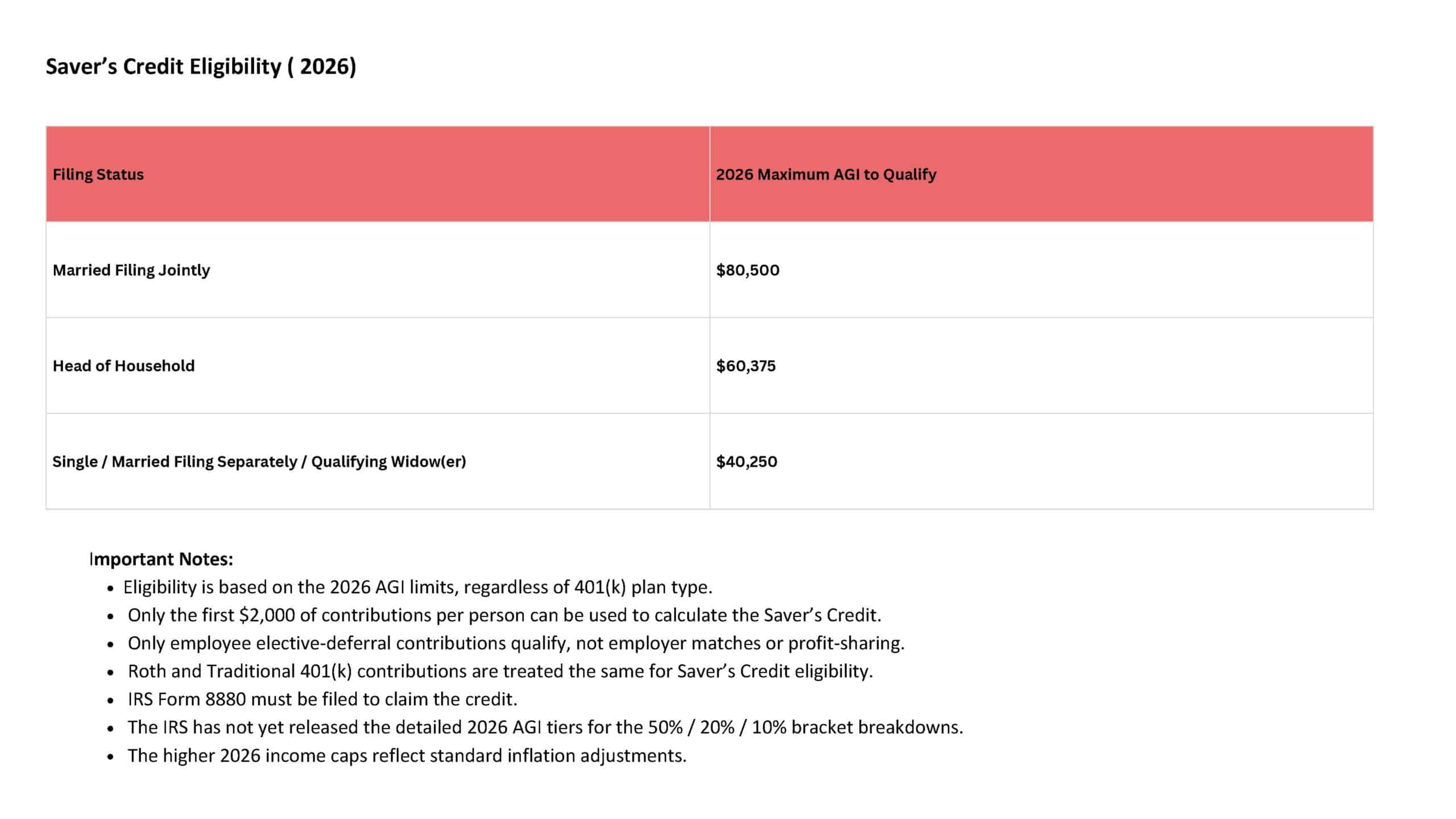

The Saver’s Credit provides a tax benefit for contributing to eligible retirement accounts, helping lower- and moderate-income earners boost their long-term savings.

Eligible Contribution Types

Employee contributions to the following accounts qualify:

• Traditional or Roth IRAs

• 401(k) plans — including Traditional, Roth, Safe Harbor, Solo/Individual, and SIMPLE 401(k)

• 403(b) plans

• 457(b) governmental plans

• SIMPLE IRAs

• SEP IRAs

(Only employee elective-deferral contributions qualify—not employer matches or profit-sharing.)

If you want to explore investment accounts that would work for your personal or retirement goals, Scarlet Oak Financial Services can be reached at 800.871.1219, or you can contact us here. To sign up for our newsletter with the latest economic news, click here.

Source:

[1] https://www.investor.gov/additional-resources/retirement-toolkit/employer-sponsored-plans/traditional-and-roth-401k-plans

[2] https://www.investor.gov/sites/investorgov/files/2019-02/Saving-and-Investing.pdf

[3] https://www.finra.org/investors/learn-to-invest/types-investments/retirement/401k-investing/investing-your-401k

[4] https://www.kiplinger.com/retirement/retirement-planning/602191/401k-contribution-limits-for-2021

[5] https://www.bankrate.com/retirement/401k-contributions/

[6] https://www.irs.gov/newsroom/irs-announces-changes-to-retirement-plans-for-2022

[7] https://www.irs.gov/newsroom/401k-limit-increases-to-23000-for-2024-ira-limit-rises-to-7000#:~:text=Highlights%20of%20changes%20for%202024,to%20%247%2C000%2C%20up%20from%20%246%2C500.

[8] https://www.irs.gov/newsroom/401k-limit-increases-to-23000-for-2024-ira-limit-rises-to-7000

[9] https://www.investopedia.com/articles/personal-finance/120315/what-good-401k-match.asp

[10] https://www.investopedia.com/articles/personal-finance/112315/how-401k-matching-works.asp

[11] https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-401k-and-profit-sharing-plan-contribution-limits

[12] https://www.gobankingrates.com/retirement/401k/is-money-401k-really-vesting-works/

[13] https://www.investopedia.com/terms/e/erisa.asp

[14] https://www.thebalance.com/how-to-withdraw-money-from-a-401-k-or-ira-2894212

[15] https://www.forusall.com/401k-blog/401k-nondiscrimination-testing/

[16] https://smartasset.com/retirement/what-are-401k-fees

https://www.investopedia.com/terms/1/401kplan.asp

[17] https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-required-minimum-distributions-rmd

[18] https://www.tiaa.org/public/support/faqs/required-minimum-distributions

[19] https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-loans

[20] https://www.fool.com/retirement/plans/401k/income-limits/

[21] https://www.irs.gov/pub/irs-drop/n-22-55.pdf

[22] https://www.irs.gov/pub/irs-drop/n-23-75.pdf

https://www.investopedia.com/ask/answers/roll-into-403b.asp

https://www.merrilledge.com/ask/retirement/rollover-a-403b-to-ira-retirement-account

https://www.investopedia.com/ask/answers/100314/what-difference-between-401k-plan-and-403b-plan.asp

https://www.investopedia.com/retirement/401k-contribution-limits/

https://www.irs.gov/newsroom/401k-limit-increases-to-23500-for-2025-ira-limit-remains-7000

https://www.irs.gov/pub/irs-drop/n-25-67.pdf

https://www.irs.gov/newsroom/401k-limit-increases-to-24500-for-2026-ira-limit-increases-to-7500

This material has been prepared for informational purposes. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on individual circumstances.