When investing in a mutual fund, you may have the opportunity to choose among several share classes, most commonly Class A, Class B, and Class C. This multi-class structure offers you the opportunity to select a share class that is best suited to your investment goals. The only differences among these share classes typically revolve around how much you will be charged for buying the fund, when you will pay any sales charges that apply, and the amount you will pay in annual fees and expenses.

investing in a mutual fund, you may have the opportunity to choose among several share classes, most commonly Class A, Class B, and Class C. This multi-class structure offers you the opportunity to select a share class that is best suited to your investment goals. The only differences among these share classes typically revolve around how much you will be charged for buying the fund, when you will pay any sales charges that apply, and the amount you will pay in annual fees and expenses.

Understanding fees and expenses

Before you can compare share classes, you need to understand the costs that are associated with mutual funds, since these costs are usually deducted from the money you’ve invested and can affect the return of your investment over time.

Typically, mutual fund costs consist of sales charges and annual expenses. The sales charge, often called a load, is the broker’s commission deducted from your investment when you buy the fund or when you sell it. The annual expenses are asset-based fees that cover the fund’s operating costs, including management fees, service fees, and 12b-1 fees (which cover distribution and marketing expenses). The expenses are generally computed as a percentage of your assets and then deducted from the fund before the fund’s returns are calculated.

So which share class should you choose? The answer to that depends on two factors: how much you want to invest and your investment time horizon.

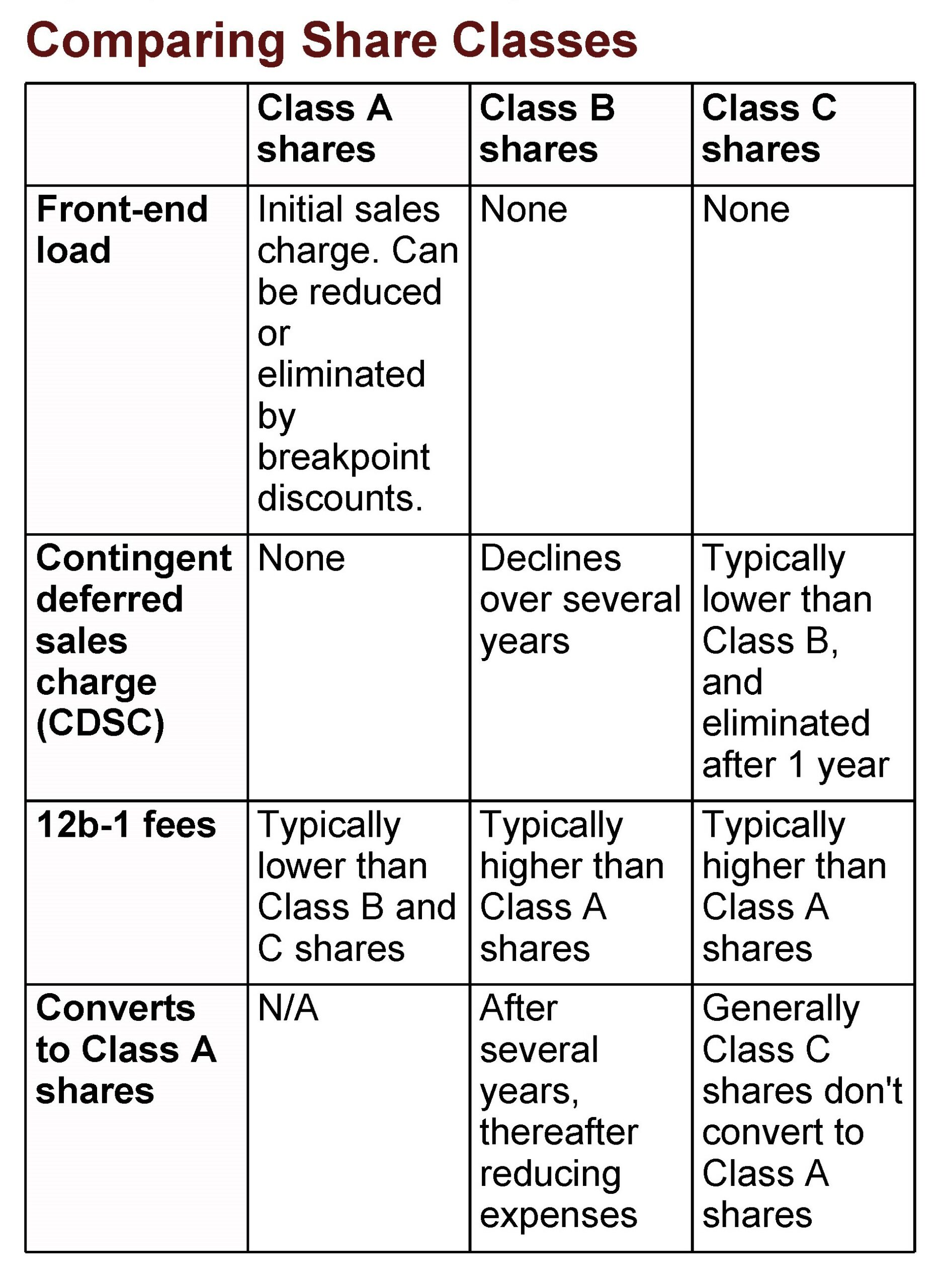

Class A shares

Class A shares may appeal to you if you’re considering a long-term investment in a large number of shares. When you purchase Class A shares, a sales charge, called a front-end load, is typically deducted upfront, reducing the amount of your investment. Suppose you decide to spend $35,000 on Class A shares with a hypothetical front-end 5% sales load. You will be charged $1,750, and the remaining $33,250 will be invested.

However, Class A shares also offer you discounts, called breakpoints, on the front-end load if you buy shares in excess of a certain dollar amount. Typically, a fund will offer several breakpoints; the more you invest, the greater the reduction in the sales load. For example, a mutual fund may charge a load of 5% if you invest less than $50,000, but reduce that load to 4.5% if you invest at least $50,000 but less than $100,000. This means that if you invest $49,000, you’ll pay $2,450 in sales charges, but if you invest $50,000 (i.e., you reach the first breakpoint), you’ll pay only $2,250 in sales charges.

You may also qualify for breakpoint discounts by signing a letter of intent to purchase additional shares within a certain period of time (generally 13 months), or by combining your current purchase with other investment holdings that you, your spouse, and/or your children have within the same fund or family of funds (called a right of accumulation). Since rules vary, read your fund’s prospectus to find out how you may qualify for available breakpoint discounts, or contact your financial professional for more information.

You may also qualify for breakpoint discounts by signing a letter of intent to purchase additional shares within a certain period of time (generally 13 months), or by combining your current purchase with other investment holdings that you, your spouse, and/or your children have within the same fund or family of funds (called a right of accumulation). Since rules vary, read your fund’s prospectus to find out how you may qualify for available breakpoint discounts, or contact your financial professional for more information.

Also, 12b-1 fees on Class A shares tend to be lower than those of other share classes, reducing your overall costs. This may make Class A shares more attractive if you wish to hold the fund for a long time.

Class B shares

Although Class B shares are becoming less common, they may still appeal to you if you wish to invest a smaller amount of money for a long period of time. Unlike Class A shares, there is no up-front sales charge, so all of your initial investment is put to work immediately. Instead, Class B shares have a back-end load, often called a contingent deferred sales charge (CDSC), that you pay when you sell your shares. The load usually decreases over time (typically 6 to 8 years), although this varies from fund to fund. By the end of the time period no sales charge applies. At that stage your shares may convert to Class A shares.

For example, suppose you invest $5,000 in Class B shares, with a 5% CDSC that decreases by 1% every year after the second year. If you sell your shares within the first year, you will pay 5% of the value of your assets or the value of the initial investment, whichever is less. If you hold your shares for 8 years, the CDSC may be reduced to zero.

Before you purchase Class B shares, however, make sure that this investment fits in with your overall goals. Class B 12b-1 fees can be considerably higher than those for Class A shares, so the cost of investing large amounts over time might be more than you would like. In addition, you don’t benefit from the breakpoint discounts available with Class A shares, and you must pay the CDSC if you sell your Class B shares within the time limit. You should also keep track of when your shares convert to Class A shares, especially if your account has been transferred from one broker to another.

Class C shares

When you purchase Class C shares, a front-end load is normally not imposed, and the CDSC is generally lower than for Class B shares. This charge is reduced to zero if you hold the shares beyond the CDSC period (typically 12 months). For those reasons Class C shares may be appropriate if you have a large amount to invest and you intend to keep the fund for less than 5 years.

However, the 12b-1 fees are greater for Class C shares than for Class A shares. Unlike Class B shares, these expenses will not decrease during the life of the investment, because C Class shares generally don’t convert to Class A shares. Also, no breakpoints are available for large purchases.

Choosing the right mutual fund share class can make a significant difference in your investment returns over time. Our firm can help you understand the different types of mutual fund share classes and determine which one is best for your investment goals. Don’t hesitate to contact us to learn more about mutual fund share classes and how we can help you achieve your financial objectives.Scarlet Oak Financial Services can be reached at 800.871.1219 or contact us here. Click here to sign up for our weekly newsletter with the latest economic news.

Source:

Broadridge Investor Communication Solutions, Inc. prepared this material for use by Scarlet Oak Financial Services.

Broadridge Investor Communication Solutions, Inc. does not provide investment, tax, legal, or retirement advice or recommendations. The information presented here is not specific to any individual’s personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on individual circumstances. Scarlet Oak Financial Services provide these materials for general information and educational purposes based upon publicly available information from sources believed to be reliable — we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.