Introduction

Homeowners insurance policies come in several standardized forms, each designed to meet the needs of specific types of property owners and dwellings. Insurance companies widely adopt these forms and provide varying levels of property coverage while maintaining consistent liability protection. Understanding the distinctions between named perils and open perils coverage, as well as the policy forms available for houses, condominiums, cooperatives, and rentals, can help you make an informed decision about the coverage that best suits your property and risk tolerance.

What is it?

Your homeowners insurance policy is most likely written on a standard form identical to homeowners policies purchased by millions of others. Even if it’s not identical, your policy is probably very similar to a standard form of homeowners policy, because insurance companies do not usually create policy forms. Instead, they adopt policy forms created by national organizations or legislative committees. In some cases, insurance companies are required by law to use a standard form for their policies.

Most of your homeowners policy consists of preprinted pages that are not tailored to your situation. The information specific to your situation is shown on your policy’s Declarations Page. Use this resource as a learning tool, but always read your policy carefully to familiarize yourself with the details of your coverage.

Overview

There are six different types of policy forms for homeowners insurance. The forms offer identical liability coverage but differ with respect to property coverage (basic named perils, broad named perils, or open perils) and dwelling type (house, apartment, condominium, or cooperative). It’s easy to determine which policy form you purchased, because each type is identified by a number:

- HO-1 Basic named perils

- HO-2 Broad named perils

- HO-3 Open perils

- HO-4 Apartments

- HO-6 Condominiums or cooperatives

- HO-8 Older homes

Although it’s not apparent from the above list, HO-1, HO-2, HO-3, and HO-8 all apply to houses, not apartment, condo, or co-op units. HO-4 and HO-6–which do apply to apartment, condo, and co-op units–are based on broad named perils coverage (see Table of Information). Tenants, as well as condo and co-op owners, need different forms because they do not own their residences and therefore cannot purchase dwelling coverage.

Basic named perils coverage

This coverage is also commonly referred to as “basic coverage.” The 11 conditions, actions, and events that are included in basic coverage are considered to be “perils” because they cause financial loss. The 11 perils are:

- Fire or lightning

- Windstorm or hail

- Explosion

- Riot or civil disturbance

- Aircraft

- Vehicles (as long as they’re operated by nonresidents)

- Smoke (not including smoke from fireplaces)

- Vandalism or malicious mischief

- Theft

- Broken glass (up to a $100 limit)

- Volcanic eruption

None of the six policy forms offers less than basic coverage. That’s because broad named perils coverage and open perils coverage provide protection for the 11 basic named perils and more. Your policy is most likely not written to provide basic coverage. Basic coverage is provided by Form HO-1, which is rarely used, and Form HO-8, which applies only to special situations.

Broad named perils coverage

This coverage is also commonly referred to as “named perils coverage.” It is similar to basic coverage in that certain perils are specifically named or listed in the policy, but it is more expansive. Named perils coverage includes the 11 perils covered by basic coverage and adds 6 more perils:

- Falling objects

- Weight of ice, snow, or sleet

- Accidental discharge or overflow of water

- Sudden and accidental tearing apart

- Freezing

- Artificially generated electrical damage

Named perils coverage also expands coverage for:

- Smoke (to include smoke from fireplaces)

- Vehicles (to include damage caused by resident-operated vehicles)

- Broken glass (to remove the $100 limit on coverage)

Named perils coverage is the coverage type most frequently featured in the six policy forms. Because the named perils are described in detail, this type of coverage features just a few, straightforward exclusions. If your policy features named perils coverage, you are not covered by property insurance for damage or destruction caused by:

- Enforcement of building codes and similar laws

- Earthquakes

- Flooding

- Power failures

- Neglect (meaning your failure to take reasonable steps to protect your property)

- War

- Nuclear hazard

- Intentional acts

Open perils coverage

This type of coverage is also known as “all risk” coverage. That’s because Form HO-3 broadly states that it covers you “against [all] risk of direct loss to property described in Coverages A [dwelling] and B [other structures].” Instead of naming the perils covered by the policy, the question of what perils are covered is left unanswered or “open.” But don’t let the label fool you. Form HO-3 (the only form to feature open perils coverage) comes complete with a lengthy list of exclusions from coverage to ensure that your insurance company is not liable for every peril under the sun.

The starting point for the exclusions from open perils coverage is the eight exclusions most frequently associated with named perils coverage (meaning losses arising from building code enforcement, earthquakes, flooding, etc.). Then there are additional exclusions:

- Freezing pipes and systems in vacant dwellings

- Damage to foundations or pavements from ice and water weight

- Theft from a dwelling under construction

- Vandalism to vacant dwellings

- Latent defects, corrosion, industrial smoke, pollution

- Settling, wear, and tear

- Pets, other animals, and pests

- Weather conditions that aggravate other excluded causes of loss

- Government and association actions

- Defective construction, design, and maintenance

Choosing between coverage types

As noted, it is unlikely that you will have the option to choose basic coverage. Form HO-1 is not available in most states (which is unfortunate as far as your wallet is concerned, because it’s the least expensive policy form), and HO-8 applies only in special situations. Renters, as well as condo and co-op owners, must use Forms HO-4 and HO-6 in all cases.

As a home owner, your real choice is between named perils coverage (HO-2) and open perils coverage (HO-3). Choosing named perils coverage has an advantage, because your premium will be generally 5 percent less than that for open perils coverage. The disadvantage of named perils coverage is that it’s less comprehensive than open perils coverage, so there are situations when HO-3 covers you but HO-2 does not. Keep in mind, however, that HO-2 does cover you for many of the most common perils that are out there. It’s a tough choice. If you’re looking to save money while obtaining solid coverage, consider purchasing a named perils policy. However, if you’re looking for the most protective policy money can buy, consider an open perils policy. Raise the question with your insurance agent when you are shopping around for homeowners insurance, and listen carefully to the answer.

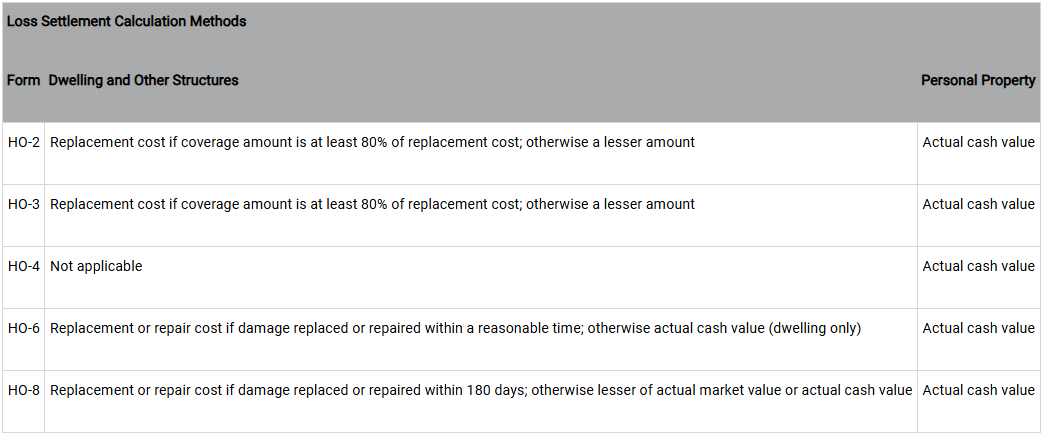

Loss settlement

Your policy contains a paragraph describing the amount you can expect to receive from your insurance company if a covered loss occurs. There are three options for calculating payment:

- Actual cash value, meaning the amount necessary to replace or rebuild the property less depreciation

- Replacement cost, meaning the amount necessary to replace or rebuild the property using similar materials

- Market value, meaning the value of the property in the real estate market at the time of loss

Payments for Coverages A and B (Dwelling and Other Structures) are typically calculated using a different method than payment for Coverage C (Personal Property). The calculation method also differs depending on the policy form.

Keep in mind that all calculation methods are still subject to the coverage limits set forth on the Declarations Page of your policy. This means you’ll never receive more than the applicable coverage limit even if replacement cost, actual value, or market value is greater.

Read the “Loss Settlement” paragraph in your policy’s “Section I–Conditions” to obtain more details concerning payment calculation methods.

Conclusion

Choosing the right homeowners insurance policy form is an important step in protecting your home and personal property. Each form offers a different combination of coverage options and exclusions based on dwelling type and risk exposure. By understanding the coverage structure, the method of loss settlement, and the differences between basic, broad, and open perils policies, you can select a policy that provides the appropriate balance of protection and cost. Reviewing your needs with a knowledgeable insurance agent will ensure you secure the right policy form for your home and lifestyle.

Scarlet Oak Financial Services can be reached at 800.871.1219 or contact us here. Click here to sign up for our weekly newsletter with the latest economic news.

Source:

Broadridge Investor Communication Solutions, Inc. prepared this material for use by Scarlet Oak Financial Services.

Broadridge Investor Communication Solutions, Inc. does not provide investment, tax, legal, or retirement advice or recommendations. The information presented here is not specific to any individual’s personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on individual circumstances. Scarlet Oak Financial Services provide these materials for general information and educational purposes based upon publicly available information from sources believed to be reliable — we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.